Social

There has been much discussion as of late on the Canadian liquefied natural gas (LNG) industry, and whether it will help lower emissions abroad, or simply add to the growing global climate change problem.

The aim of this piece is to try to set the record straight and broaden the conversation to a global context. Full disclosure, this post is long, mainly because I want you, the reader, to better understand not only the magnitude of the challenge that we face in lowering global emissions, but also what we as Canadians can do about it.

I cannot say that this narrative is my own. I have merely tried to bring together various stories written by some equally passionate individuals; individuals who are not just passionate about the problem of climate change, but passionate about the practical solutions we have in front of us.

Let me begin by first summarizing the main arguments made against Canadian LNG development:

- The amount of methane that leaks during the natural gas production process negates the environmental benefit of burning natural gas over coal.

- The emission reductions from Canadian LNG displacing coal are overstated.

- LNG exports may end up displacing renewable energy, making the challenge of reducing global emissions even harder.

- Canada should focus on the climate commitments it made under the Paris Agreement in 2015 and not consider its emissions in a global context.

However well-intentioned these arguments may be, they do not hold up once all the facts are examined.

An extensive peer-reviewed Canadian study has shown conclusively that Canadian LNG exports will provide large emission reductions on a global scale; and once built, Canada’s fleet of LNG export facilities will be greenest in the world (more on this below).

Simply put, growing Canadian LNG exports is necessary if the world is to meet its Paris commitments of keeping global warming well below 2 degrees Celsius.

To understand why this is the case, we must first step outside of our provincial and Canadian mindsets and understand that the most immediate and critical goal to meaningfully reduce global emissions is to actively encourage and enable the substitution of coal in the power and industrial sectors of Asian emerging economies.

Renewable energy, despite its record-breaking pace of development, will not be able to displace coal in emerging economies on its own in the time that the Intergovernmental Panel on Climate Change (IPCC) – the United Nations body that assess climate change related science – estimates we have to reduce emissions (more on this below).

The world is not in a race to renewables, but a race to reduce emissions.

This is the original goal, and we must get back to this mindset.

From an environmental perspective, coal is the most carbon-intensive fossil fuel in our global energy mix and is responsible for 40 per cent of global annual carbon dioxide (CO2) emissions. Coal is predominantly used in the power sector to generate electricity, especially in emerging economies in Asia where annual use is ramping up at an alarming rate.

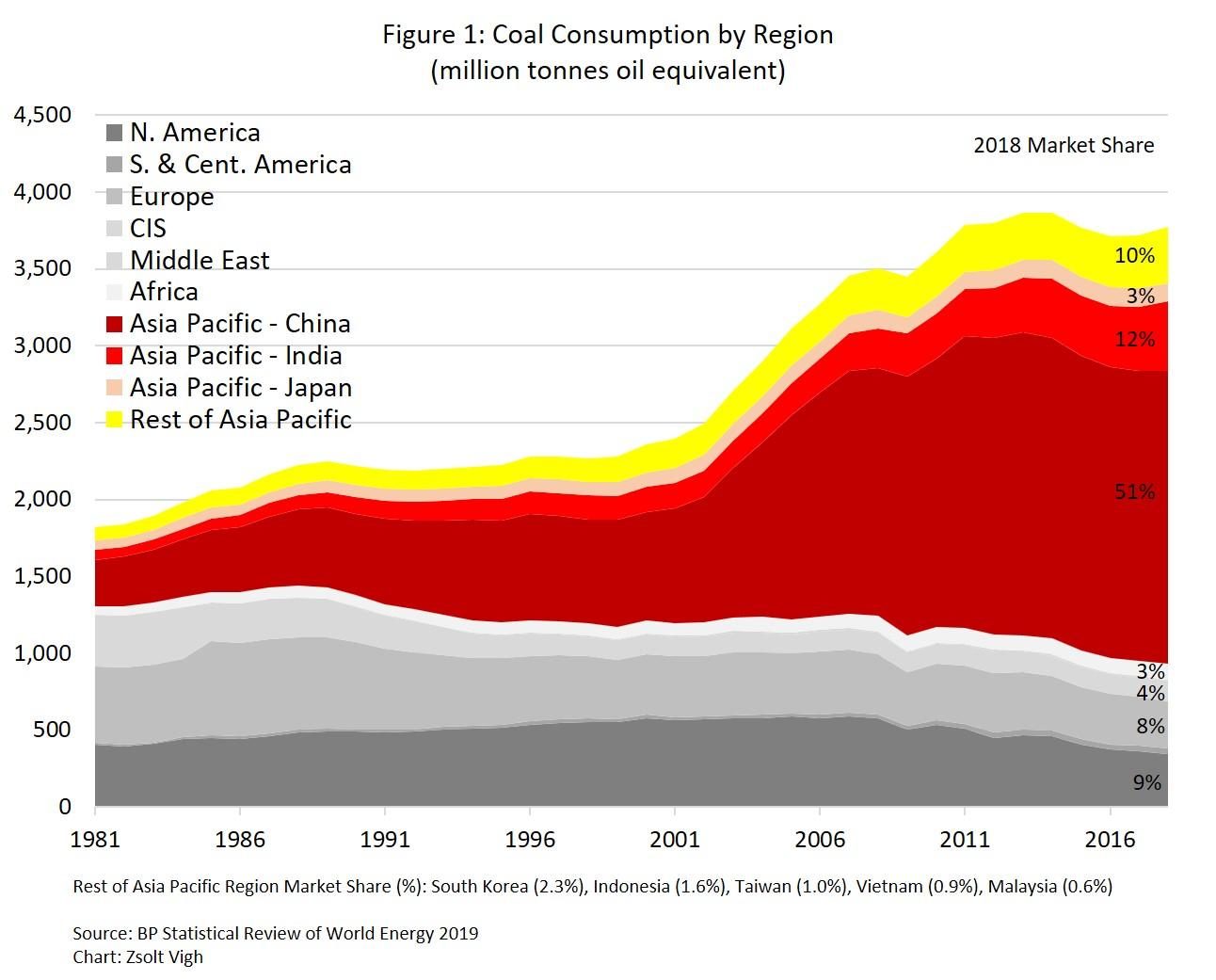

I would like to provide a quick note on Figure 1 so readers can better understand the scale of coal use worldwide. The unit of measurement in the figure is “million tonnes of oil equivalent”, which truth be told is a difficult term for anyone to wrap their head around. In more practical terms, the amount of energy contained in one million tonnes of oil is the equivalent annual energy output from a smaller nuclear power plant, like the Callaway nuclear power generation facility, or the equivalent annual energy output from 2,000 (2.5 MW) wind turbines. Using these new metrics, we can start to better understand the scale of the problem.

As seen in Figure 1, the Asia Pacific region now consumes 75 per cent of the world’s annual coal production. China uses more coal every year than the rest of the world combined, India (the world’s second-largest consumer of coal) grew consumption at 9 per cent last year, and major developing countries in Southeast Asia (Indonesia, Malaysia, Pakistan, Philippines, and Vietnam) as a group have increased their coal use on average 9 per cent a year since 2015, a pace at which by the early 2020s, if continued, will vault them ahead of the combined coal use of Japan and South Korea (the fourth and fifth largest consumers of coal in the world).

If the world is to take immediate and meaningful action to reduce green house gas (GHG) emissions, the decarbonization of the power sector in Asian emerging economies through the active substitution of coal needs to be the number one priority.

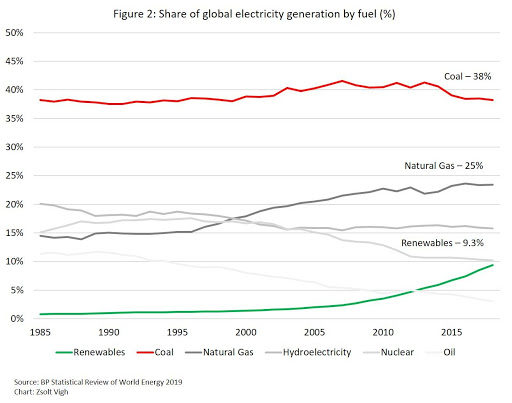

The power sector, due to its reliance on coal as its main fuel source, is the single largest contributor to global GHGs (the power sector represents about 38 per cent of total global annual carbon dioxide emissions or 13,000 million tonnes per year). Coal generates twice as much GHGs as natural gas (as cited on page 19 of the 2012 IPCC Special Report) and can produce a significant amount of microparticulate matter, mercury, and other pollutants that are all harmful to human health and the environment.

Decarbonizing the power sector has proven to be a major challenge globally for two main reasons:

1) Robust global growth of power demand due to the shift towards electrification.

Renewable capacity build-out has not been able to decarbonize the existing power generation fleet and keep up with new power demand at the same time. In 2018, global power demand growth clocked in at 3.7 per cent, one of the strongest growth rates seen in the past 20 years and almost entirely driven by developing Asia. In fact, despite a $4 trillion (US) investment in renewable power since 2005, coal use in the global power fuel mix remains stubbornly flat at 38 per cent, the same share as 20 years ago (Figure 2).

2) The inability of renewable energy to act as baseload power due to weather intermittency and the lack of any cost-effective grid-scale battery technology.

When the wind doesn’t blow and the sun doesn’t shine, renewables cannot generate power and a backup source is needed to offset the loss in energy supply to the grid. In Asia, this backup power source is most often coal-fired power generation (and in China and India, the two largest emitters in Asia, this is almost exclusively the case).

For example, in 2017 China’s wind and solar power capacity represented 16.5 per cent of its total electricity fuel mix, yet wind and solar only generated 6.5 per cent of the country’s total power due to the combined capacity factor of these two resources being only 18%. In other words, wind and solar assets were only generating power at full capacity 18% per cent of the time; as a result, coal-fired power generation had to ramp up to during the 82% per cent of the time when renewables aren’t generating power to meet grid demand, greatly reducing the net emission reductions achieved.

Contrary to popular headlines in the press, there are currently no cost-effective and grid-scale battery options to significantly increase the use of renewable energy, and anything feasible is still years away. For example, a recent MIT study estimated, that even with another 30 per cent drop in costs, a large-scale battery build-out in the U.S. would cost $2.5 trillion (US). In the words of Bill Gates:

“There’s no battery technology that’s even close to allowing us to take all of our energy from renewables and be able to use battery storage in order to deal not only with the 24-hour cycle but also with long periods of time where it’s cloudy and you don’t have sun or you don’t have wind.”

Simply put, renewable energy, despite its record-breaking pace of development, will not be able to displace coal in emerging economies on its own in the time that the IPCC estimates that we have to reduce emissions.

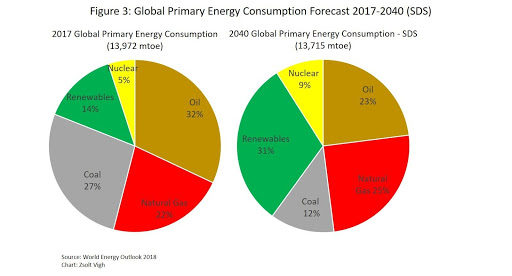

What does meeting the Paris Climate commitments look like on a global scale? The independent, Paris-based International Energy Agency (IEA) has developed a Sustainable Development Scenario (SDS) that is consistent with reducing GHGs and limiting global warming to well below 2 degrees Celsius.

In this scenario, between 2017 and 2040, world energy usage remains flat, natural gas and renewables grow their market share to 25 per cent from 22 per cent to 25 per cent and to 31 per cent from 14 per cent, to 31 per cent respectively, and coal use plummets to 12 per cent from 27 per cent to 12 per cent of the total world energy mix (Figure 3).

In the SDS, natural gas is the only hydrocarbon that grows in demand out to 2040, and this is for two main reasons:

1) Natural gas is the cleanest-burning fossil fuel, emits half as much GHGs as coal, and can readily displace coal-fired power plants that currently serve as baseload power and the backup power source for renewable energy in most of developing Asia.

2) Natural gas can support renewable energy development as it can serve as the backup source of power generation when the wind doesn’t blow, and the sun doesn’t shine.

Natural gas is particularly important in the Asia-Pacific region, the primary market that Canadian LNG is poised to serve.

In the SDS, natural gas use in the Asia-Pacific region doubles between 2017 and 2040, with growth led by China and India, which are expected to increase natural gas consumption by 190 per cent and 350 per cent respectively.

Today, China and India rely on coal-fired generation to generate most of their power (67 per cent and 73 per cent in 2018 respectively), with renewables only making up 9 per cent and 8 per cent respectively of each country’s total yearly power consumption. As China and India align their energy systems to achieve less than 2-degree Celsius warming over the next two decades, natural gas use drastically increases in their energy supply chain.

This huge growth in natural gas consumption makes sense as China and India move to displace coal from the industrial sector with natural gas (renewable power isn’t an option here) and from the power generation sector with a combination of natural gas and renewables.

Renewables in the SDS already ramp up aggressively, going from 14 per cent to 31 per cent of the total world energy mix in 20 years (Figure 3), but renewables will need a backup power source for the foreseeable future (due to the lack of cost-effective large grid-scale batteries).

As natural gas use in China and India’s energy systems increases, it will compete against coal for the role of baseload power and backup power for renewables. Without natural gas, legacy coal hangs on as the backup to renewables (and coal generates twice as much GHGs as natural gas on a lifecycle basis).

Coal is competing against the combination of natural gas and renewables, that is the market dynamic.

As China and India decarbonize their energy systems, natural gas becomes even more important than before in the global fight to reduce emissions.

If China and India need to drastically grow their natural gas use, where will the additional supply come from? One word: LNG.

China and India will have to rely on LNG imports as they do not have the domestic natural gas reserves to meet today’s demand, let alone tomorrow’s. Between 2017 and 2018, gas consumption in China increased by 20 per cent and LNG imports fueled 53 per cent of this new demand. In fact, China has doubled its LNG import volumes in the last two years and by 2024, China is set to become the world’s largest LNG importer.

In the words of Yao Li, CEO of the Chinese energy consulting firm SIA Energy: ,

“Demand [for LNG in China] is almost infinite.”

India has also been actively expanding its LNG import capabilities, with import volumes expected to double in four years. In fact, India’s Ministry of Petroleum and Natural Gas recently announced that it plans to invest $60 billion (US) over the next five years to develop the country’s gas distribution infrastructure, including pipelines and LNG import terminals.

As countries in the Asian-Pacific region move to align their energy systems to achieve less than 2-degree Celsius warming, natural gas use will drastically increase in their energy supply chains.

There exists a significant market opportunity for LNG exporters to meet this demand and displace coal from the power system at scale. But not all LNG is created equal; some LNG sources have higher life cycle emissions than others. So how does Canadian LNG stack up?

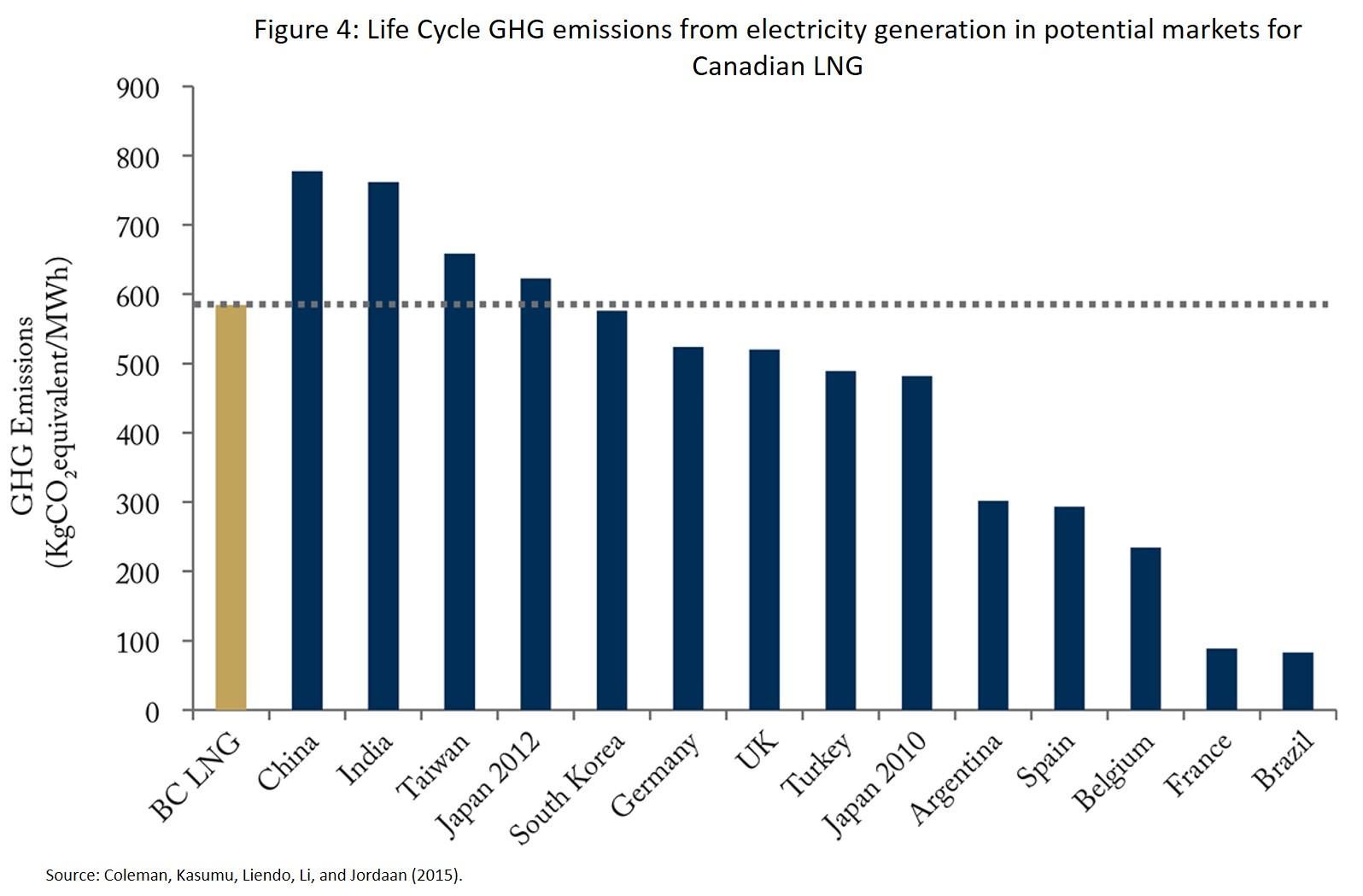

In 2018, researchers from the University of Calgary, Johns Hopkins University, the Massachusetts Institute of Technology (MIT) and Southern Methodist University released a landmark, peer-reviewed paper that analyzed the life cycle emissions from Canadian LNG and compared them to the weighted average life cycle power sector emissions of the world’s 13 major LNG importing countries.

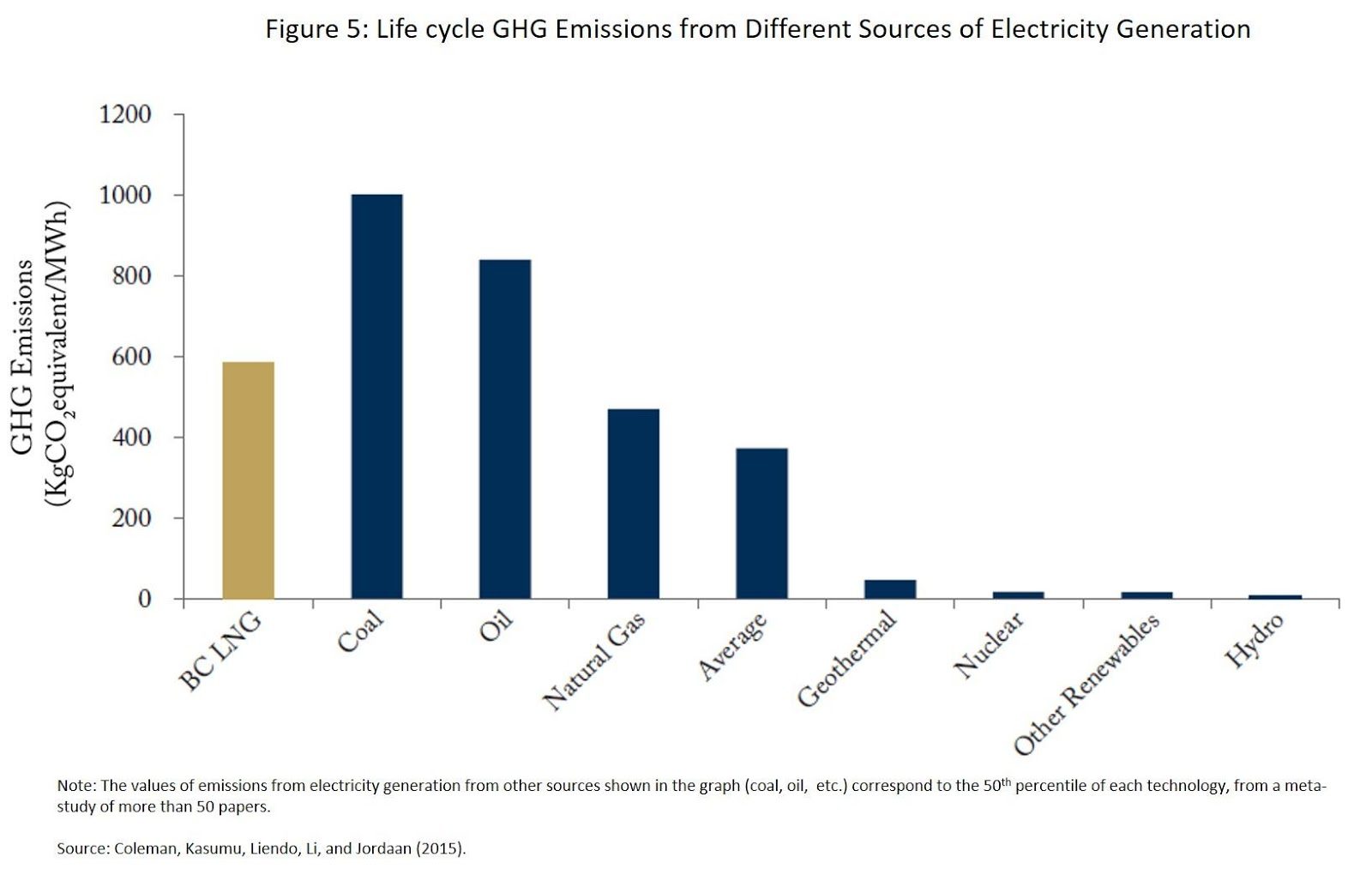

The authors’ conclusions were that on a life-cycle basis, Canadian LNG emits 25 per cent less GHGs than the average fuel mix currently used by China and India in their respective power sectors (Figure 4) and on a direct substitution basis Canadian LNG would emit 40 per cent less GHGs than coal (Figure 5).

In the words of Rob Seeley, energy and sustainable development consultant and president of E3Merge Consulting:

“For every unit of GHGs that British Columbia produces to get that LNG to market, the overseas production of GHGs goes down by a factor of 10 … Shipping LNG at design capacity from Kitimat to displace coal-generated electricity in China would reduce global GHG emissions by 60 to 90 million tonnes annually.”

Taking the lower end of the range of potential GHG emission reductions (to be conservative), a 60 million tonne reduction in GHGs would equate to 20 per cent of Canada’s 2030 emission reduction target or the removal of 50 per cent of Canada’s cars. Keep in mind this 60 million tonne reduction will come from just one project!

Furthermore, Canada is in a unique position to deliver the most carbon competitive LNG in the world.

Once built, Shell’s LNG Canada project will beat out the world’s most GHG efficient LNG facility (The Snohvit LNG facility in Norway) by 20 per cent. What’s more, other projects under consideration (Woodfibre’s, Chevron’s, and GNL’s LNG projects) will all be powered by hydroelectricity, reducing point source emissions by up to 80 per cent.

Using hydroelectricity instead of natural gas for power generation during the natural gas to LNG conversion process is a step-change in GHG intensity (how much carbon dioxide is emitted per tonne of LNG produced), and once built, these projects will even surpass Shell’s LNG Canada project in terms of GHG efficiency.

Taken together, Canada’s fleet of LNG export facilities, once built, will be the greenest in the world.

One of the main and reoccurring arguments that has been put forward against LNG development is that the amount of fugitive methane emissions that are produced along the natural gas value chain, (the volume of natural gas that leaks out from various equipment during the production, transport and processing, of natural gas and escapes into the atmosphere), significantly increases natural gas’s GHG emissions, so much so that it is worse than coal on a life-cycle basis. This argument would certainly have merit if it were true, but in the Canadian context, this is not the case.

Before I get into why that argument is incorrect, I would like to first provide some background information so that readers understand why fugitive methane emissions matter.

To start, methane emissions are a concern because methane traps 28-86 times as much heat per unit mass compared to carbon dioxide while in the atmosphere (as cited on page 714 of the IPCC’s Fifth Assessment Report on Climate Change). Why the range in the number? While methane traps more heat than carbon dioxide while in the atmosphere, it also remains there for a much shorter time (12 years). Therefore, when converting methane emissions to carbon dioxide equivalents, the time frame matters.

The standardized time frame used by the IPCC is the 100-year global warming potential; however, calculations are also often shown with the more conservative 20-year global warming potential.

- Over a 20-year timeframe, one tonne of methane is equivalent to 84-86 tonnes of CO2

- Over a 100-year timeframe, one tonne of methane is equivalent to 28-34 tonnes of CO2

Considering the more conservative scenario (the 20-year global warming potential of methane), as long as fugitive methane emissions are less than 3 per cent of natural gas production, natural gas has lower life cycle emissions than coal.

According to the B.C. provincial government, the province’s current methane emissions leakage rate (specific to the oil and gas industry) is 0.3 per cent. Even if we take the publications written by St. Francis Xavier University or the Suzuki Foundation at face value (despite several questions about their comparability and validity), the province’s methane emissions leakage rate from oil and gas production would only increase to somewhere between 0.4 percent and 0.45 percent – far below the 3 percent breakeven threshold.

The landmark 2018 paper I cited earlier also incorporated provincial GHG emission data from 112 natural gas facilities in B.C. into its analysis and still concluded that Canadian LNG has 25 per cent lower life cycle GHG emissions than the average fuel mix of China and India, and 40 per cent lower life cycle GHG emissions than coal.

However, even if Canadian natural gas is clearly better than coal, that bar is set too low. The environmental case for Canadian natural gas should not simply depend on beating the emission performance of the most carbon intensive fuel, but rather on producing the lowest emission intensity natural gas in the world. Canadians expect government and industry to work together to ensure that energy production and environmental protection go hand in hand. And in this regard, there is action being taken on multiple fronts.

Geoscience BC, an independent non-profit organization, in conjunction with the federal government and several natural gas companies, has launched a ground breaking project called GHGMap. Running from 2017-2020, the project, which is using cutting edge drone- mounted sensor technology developed by NASA, is providing independent real-time mapping of fugitive GHG emissions. The project will dramatically improve the speed, accuracy and cost of GHG emission measurement in the field, and undoubtedly lead to further improvements related to best practices in resource development.

Furthermore, the federal government in Canada has introduced national methane regulations that will further reduce methane emissions from the oil and gas sector by 40 per cent to 45 per cent by 2025. As a result, by the time the first LNG plant is finished construction and the first shipments of LNG begin (projected to be in the 2024 to 2025 timeframe), methane emissions from natural gas will be 40 per cent to 45 per cent lower than they are today.

Major natural gas producing companies like Shell, Encana and ARC are also taking a proactive role in further reducing their GHG and methane emissions. These companies are electrifying their natural gas processing plants, designing new facilities with modern zero-methane-emitting instrumentation, and retrofitting existing facilities with similar zero-methane technologies. Using hydroelectricity instead of natural gas to power their natural gas processing plants has reduced direct GHG emissions by up to 90 per cent, and new modern zero-methane instrumentation technology has completely removed previous sources of potential methane leaks.

The electrification of the upstream and downstream processes in the LNG value chain represents a step-change in carbon intensity that is not being done anywhere else in the world.

By the time the first shipments of Canadian LNG begin, modern infrastructure will dominate the gas supply mix, and strict regulations will continue to drive the residual methane leakage rate even lower than what it is today.

When considering the whole picture, Canadian LNG is a clear climate win today and tomorrow.

Drastically reducing emissions while continuing to deliver additional energy that the developing world desperately needs represents perhaps the greatest challenge of the 21st century. The first and most meaningful step we can take as a global community is to actively encourage the substitution of coal in China, India and the developing Southeast Asian community.

Through its LNG exports, Canada has a unique opportunity to lead this effort and significantly contribute to lowering emissions abroad. While any LNG project that is built here will most certainly increase local emissions, if this country is truly committed to helping reduce emissions globally, then these projects must be analyzed in a global context. Focusing solely on Canadian emissions while ignoring important levers that could contribute to emission reductions outside our borders is incomprehensible when the stakes are so high.

We need global collaboration, cooperation is not enough.

We must not be parochial in our actions. Climate change knows no boundaries, and lowering emissions will take a collective, global effort, one that Canada should be proud to help lead.

Zsolt Vigh is a Professional Engineer who has worked in various roles across the Canadian oil sands, shale gas and LNG sectors. He completed his undergraduate degree in Chemical Engineering at the University of Calgary in 2011 and recently completed his MBA at the Richard Ivey School of Business in London, ON.

Vigh’s interests lie at the intersection of energy and the environment, and he spends his spare time researching, reading and writing about climate change, energy systems and the realities of the energy transition.

For this piece, Vigh would like to acknowledge Dr. Blair King (a Professional Chemist who blogs on energy and the environment) and Tyler Bryant (former Senior Analyst at the IEA) whose work, along with that of the IEA, BP Statistical Review, and the ARC Energy Research Institute was critical to this column.