Social

To sign up to receive the latest Canadian Energy Centre research to your inbox email: research@canadianenergycentre.ca

Download the PDF here

Download the charts here

Executive Summary

Over the past two decades, Canada’s crude oil sector has been making a growing contribution to the operations of U.S. petroleum refineries.

U.S. petroleum refineries are converting Canadian crude oil, including heavy oil, into products that people in the United States use daily, including transportation fuels (gasoline and diesel), chemicals, and plastics.

The economic impacts of the U.S. refinery industry to the American economy are substantial, including $350 billion in GDP, $539 billion in gross output, over 40,000 jobs, and nearly $74,000 in mean annual wages earned. The availability of Canadian crude oil feedstock for the U.S. refineries to process is partly responsible for the industry’s economic growth and performance.

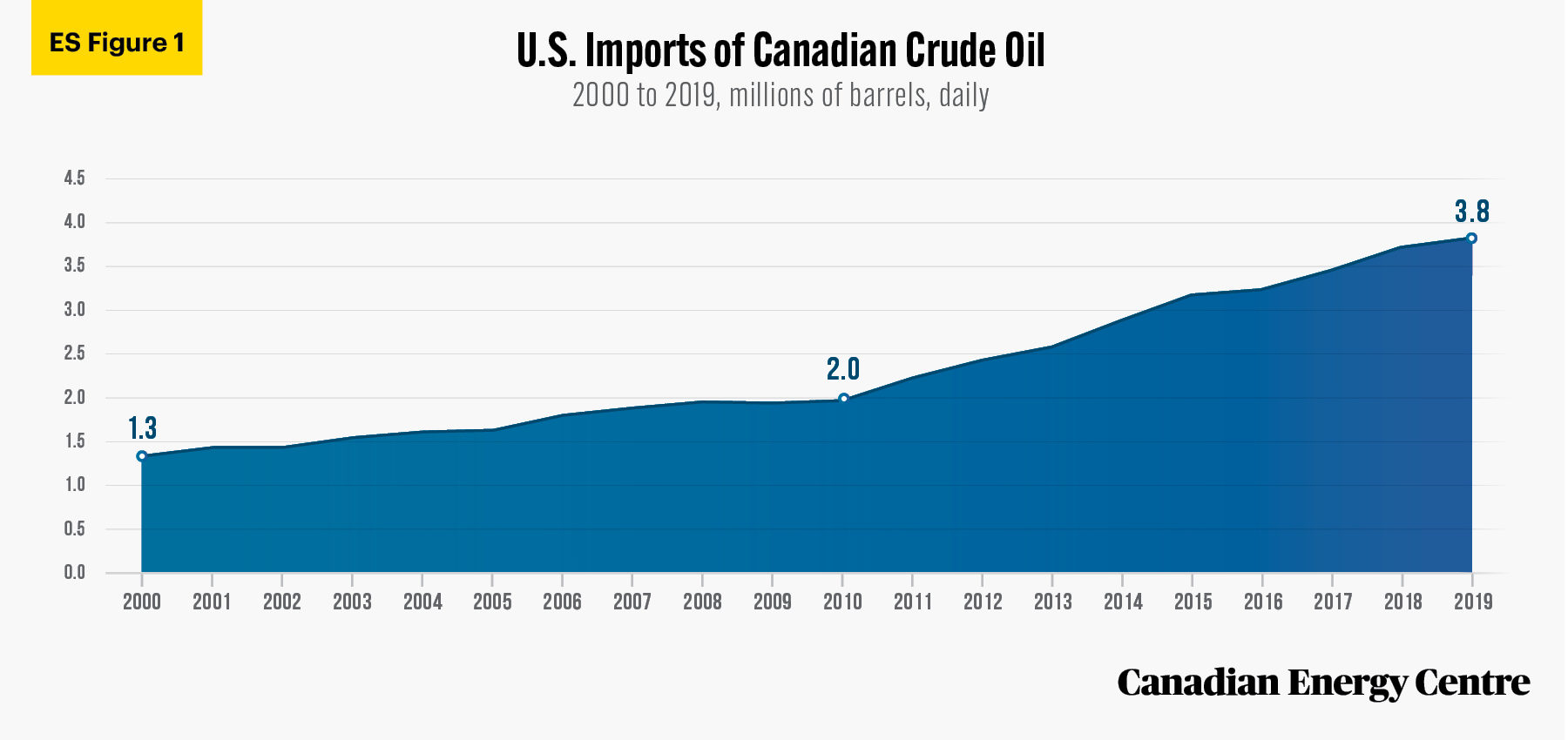

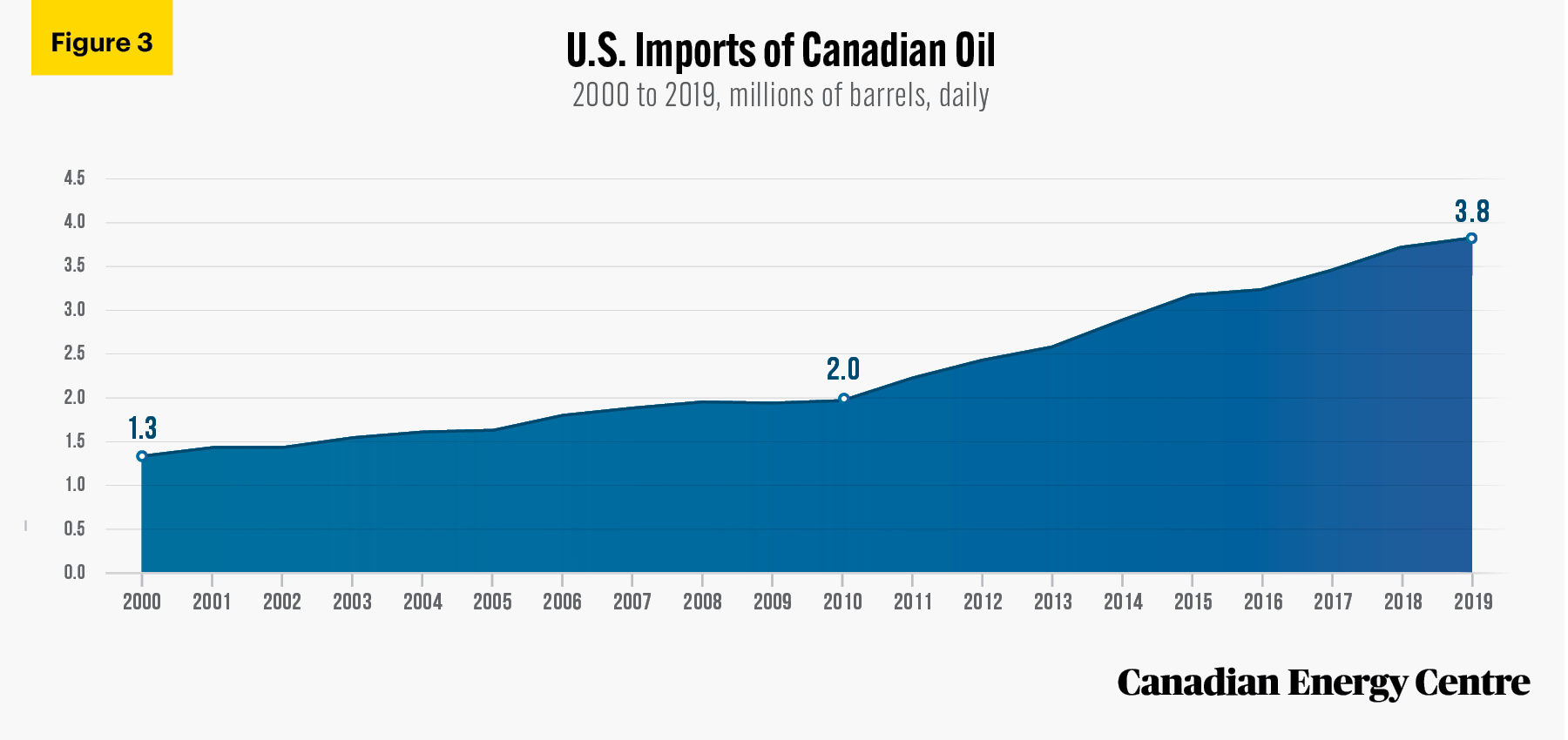

Overall, Canadian exports of crude oil to the various Petroleum Administration for Defense Districts, or PADDs, for processing have risen from over 1.3 million barrels per day in 2000 to over 3.8 million barrels per day in 2019, an increase of 183 per cent, at a time when overall U.S. oil imports fell sharply as domestic oil output increased (see Executive Summary Figure 1). Canadian crude as a proportion of U.S. refinery feedstock has steadily risen over the past two decades from nearly 9 per cent to over 22 per cent overall.

Source: US Energy Information Administration, 2020a.

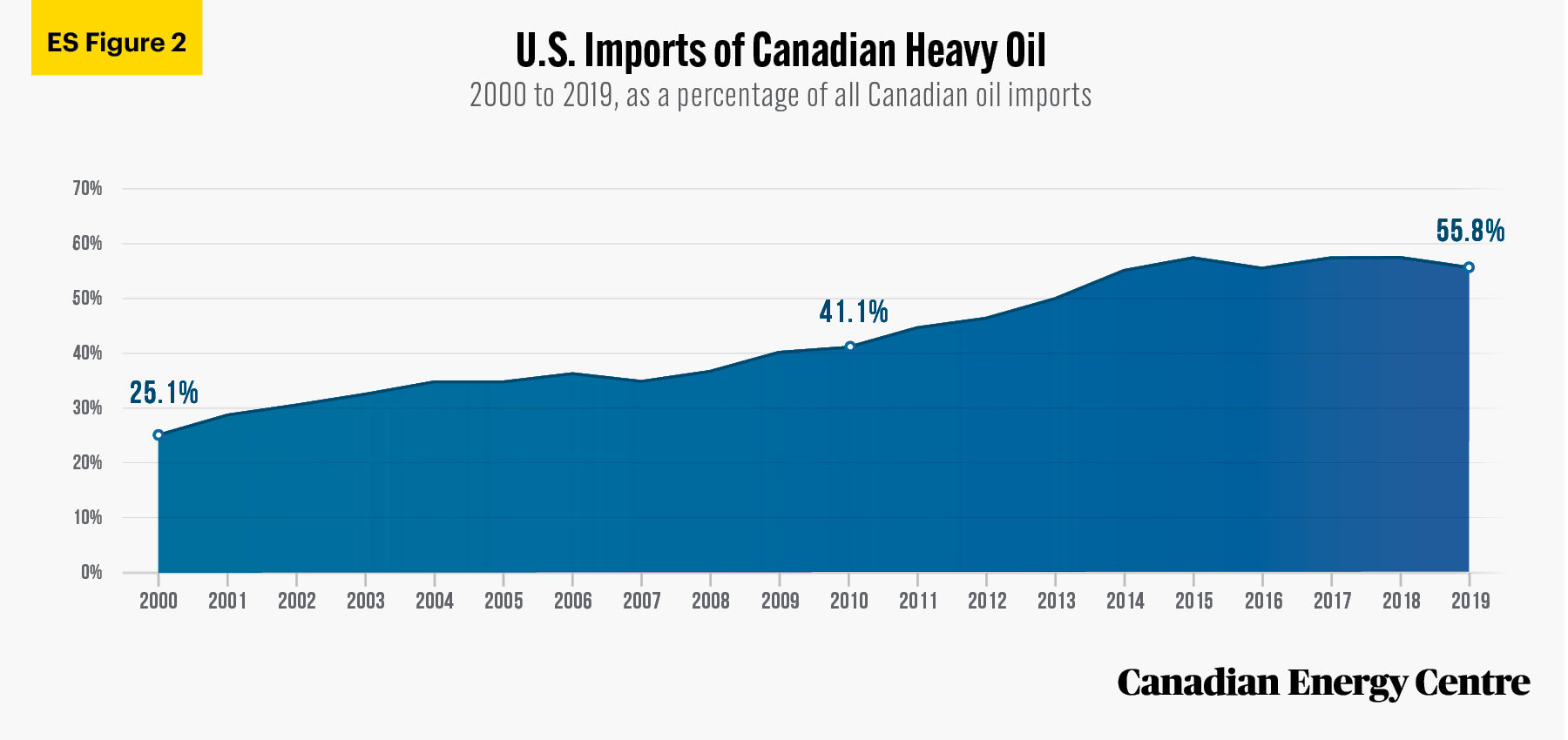

U.S. refineries are growing increasingly reliant on Canadian heavy oil, including oil from the oil sands. The total percentage of heavy crude oil that the U.S. imports from Canada as a share of all of its imports of Canadian oil has risen from 25.1 per cent in 2000 to 55.8 per cent in 2019, an increase of 122 per cent over the past two decades (see Executive Summary Figure 2).

Continuing to build pipeline infrastructure such as TMX and Keystone XL is critical to maintaining a strong U.S. refining industry and increasing Canada’s share of the crude oil the industry uses, particularly in Petroleum Administration for Defense District 3 (PADD 3), the U.S. Gulf Coast, and PADD 5, the U.S. West Coast, which are configured to process more Canadian heavy oil.

If the United States is unable to increase its refining capacity because its access to Canadian crude oil supplies fails to grow or is limited, the U.S. will turn to crude oil imports from less-free countries, which in turn will risk North American energy security.

Source: US Energy Information Administration, 2021a.

Introduction

Over the past two decades, Canada’s crude oil sector has been making a growing contribution to the operations of U.S. petroleum refineries.

Those refineries are converting Canadian crude oil, including heavy oil, into products that people in the United States use daily, including transportation fuels (gasoline and diesel), chemicals, and plastics. As noted by Oil Sands Magazine (OSM), “despite becoming more energy independent due to rising oil production, U.S. refineries are becoming increasingly more reliant on Canada’s heavy crude, which is required to meet feedstock specifications” (Oil Sands Magazine, 2020).

In this CEC Research Brief, we examine a number of metrics that illustrate the importance of Canadian crude oil, particularly heavy crude, to the operation of U.S. refineries in the five Petroleum Administration for Defense Districts (PADDs). The United States is divided into PADDs for the allocation of fuels derived from petroleum products, including gasoline and diesel fuel.

Key metrics of performance by U.S. refineries include Canadian crude oil exports processed at US refineries, the percentage of Canadian feedstock those U.S. refineries use, and how reliant they are on heavy oil with an American Petroleum Institute (API) gravity index of 25 degrees or less.¹

1. API gravity is a commonly used index for measuring the density of a crude oil or refined products. Crude oil will typically have an API between 15 and 45 degrees. The higher the API, the lighter the crude, while the lower the API, the heavier the crude.

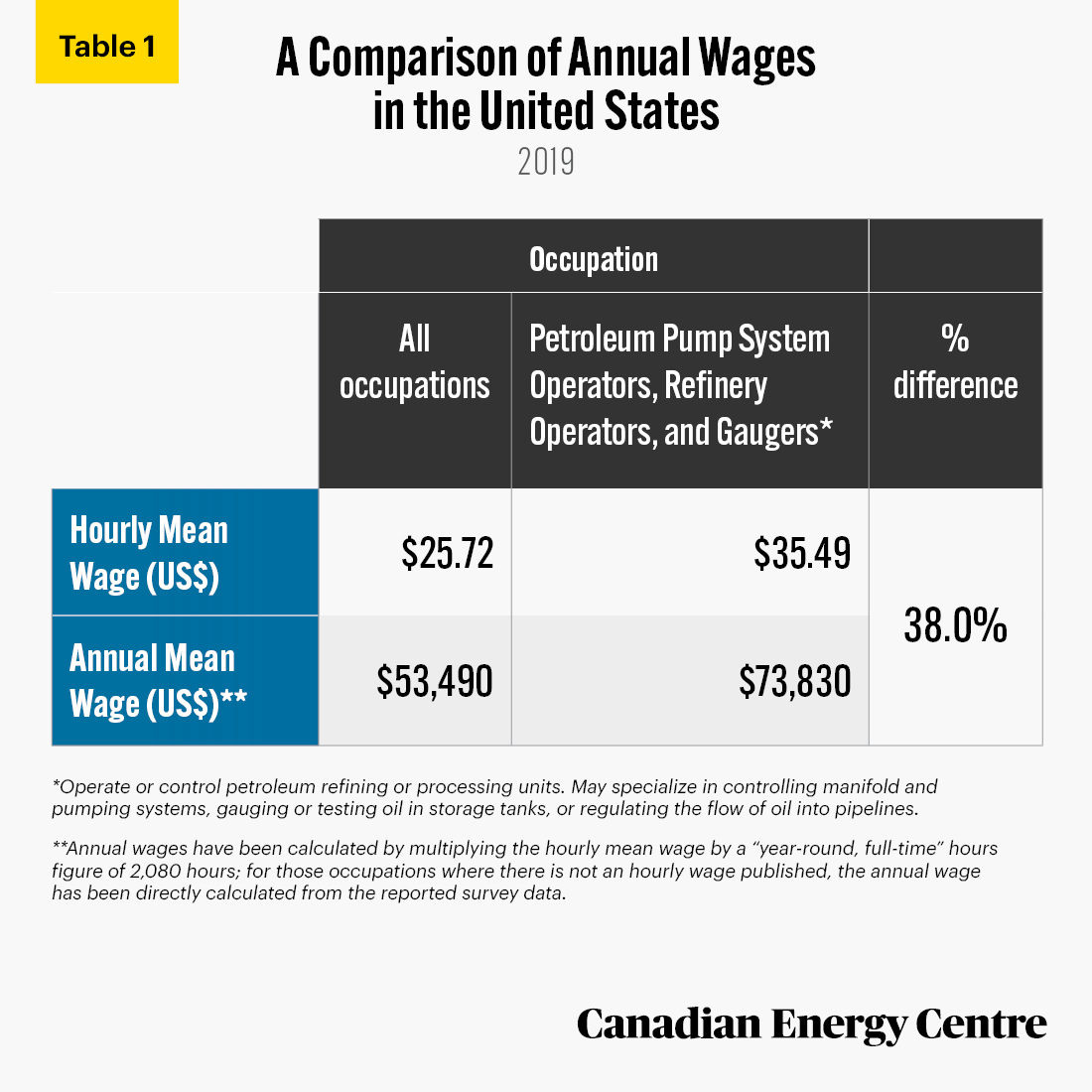

Economic impacts in the United States of U.S. refineries: $350 billion in GDP, $539 billion in gross output, over 40,000 jobs, and nearly $74,000 in mean annual wages earned

There are currently 133 petroleum refineries operating across the 5 U.S. PADDS. That includes:

- 7 in PADD 1 (U.S. East Coast);

- 25 in PADD 2 (U.S. Midwest);

- 56 in the PADD 3 (U.S. Gulf Coast);

- 16 in PADD 4 (U.S. Rocky Mountains);

- and 29 in PADD 5 (U.S. West Coast) (Oil Sands Magazine, 2020).

U.S. refineries have a significant annual impact on the American economy.

- According to IBIS World, U.S. petroleum refiners contribute about $350 billion to the American economy, annually (IBIS World, 2020).

- The gross output² of the U.S. refinery sector in 2019 was $539 billion. The refinery sector’s gross output has increased by nearly $326 billion or 153 per cent over the past two decades (U.S. Bureau of Economic Analysis, 2021).

- As of May 2019, there were 40,370 people employed in the U.S. petroleum refining industry (U.S. Bureau of Labor Statistics, 2020a).

- The annual mean wage earned in the U.S. petroleum refining industry was $73,830 as of May 2019, about 38 per cent higher than the annual mean wage earned for all occupations in the U.S. (see Table 1) (U.S. Bureau of Labor Statistics, 2020b).

2. A measure of an industry’s sales or receipts, including sales to final users in the economy and sales to other industries.

Source: U.S. Bureau of Labor Statistics, 2020a, 2020b

U.S. refining capacity reaches 17 million barrels per day in 2019

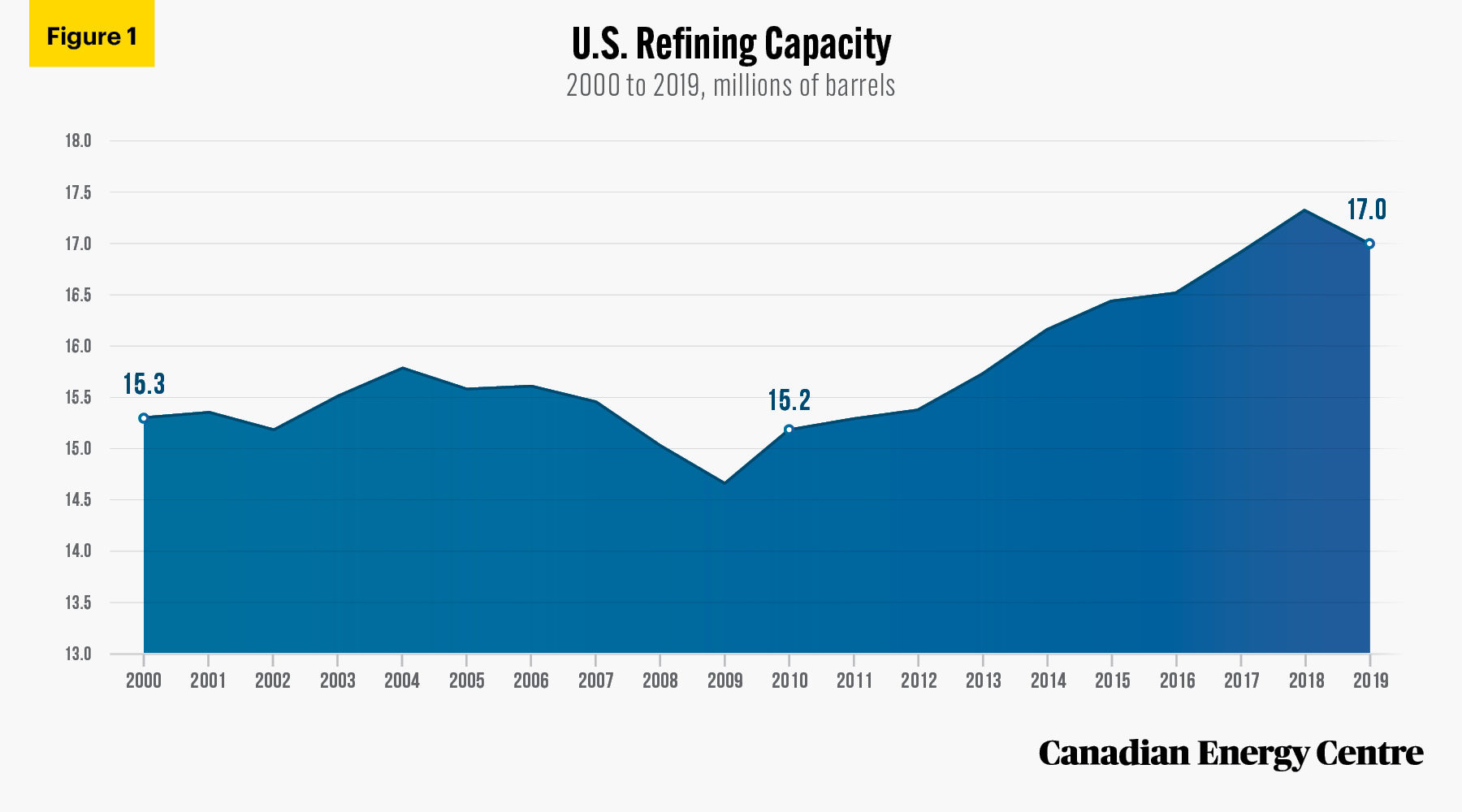

Total refining capacity in the United States has increased from 15.3 million barrels per day of crude processed in 2000 to nearly 17 million barrels per day of crude processed in 2019, an increase of over 11 per cent (see Figure 1). The increase has occurred despite the fact that no new U.S. refineries have been built. Instead, capacity has been added to existing U.S. refineries.

Source: U.S. Energy Information Administration, 2020b.

Broken down by Petroleum Administration for Defense District (see Figure 2), refining capacity in PADD 1 has fallen from 1.5 million barrels per day in 2000 to 900,000 barrels per day in 2019, a decrease of over 39 per cent. Oil Sands Magazinenotes about PADD 1 that the U.S. East Coast is largely isolated from Canada’s pipeline supply, relying mostly on seaborne crude. Most of its imports from Canada are sourced from oil platforms located offshore Atlantic Canada. (Oil Sands Magazine, 2020)

the U.S. East Coast is largely isolated from Canada’s pipeline supply, relying mostly on seaborne crude. Most of its imports from Canada are sourced from oil platforms located offshore Atlantic Canada. (Oil Sands Magazine, 2020)

PADD 2 refining capacity has increased from 3.4 million barrels per day in 2000 to 3.8 million barrels per day in 2019, an increase of 12 per cent. According to OSM,

the U.S. Midwest remains by far the largest customer for Western Canadian producers. The region is served by Enbridge’s Mainline pipeline, which is planned to be expanded to almost 3 million barrels per day. Midwest refineries blend mostly heavy crude from the oil sands, with light oil produced in North Dakota’s Bakken shale, which has also seen an increase in production. (Oil Sands Magazine, 2020)

Source: U.S. Energy Information Administration, 2021a.

PADD 3 refining capacity has increased from 7.1 million barrels per day in 2000 to 9.1 million barrels per day in 2019, an increase of nearly 28 per cent. According to OSM,

with a large refining capacity and a dwindling supply of heavy oil, PADD 3 (Gulf Coast) is a leading customer for bitumen from the oil sands. The region’s refineries are best designed to handle heavy sour grades, offering the best purchase prices for the world’s heavy oil benchmarks. The region is currently served by TC Energy’s Keystone Pipeline, with additional volumes shipped via the Midwest, or transported directly by rail. (Oil Sands Magazine, 2020)

PADD 4 refining capacity has increased from 513,000 barrels per day in 2000 to 630,000 barrels per day in 2019, an increase of nearly 23 per cent. According to OSM,

the Rocky Mountains region is located just south of Alberta and is the smallest of all five U.S. crude processing areas. PADD 4 relies heavily on heavy sour crude from the oil sands, blended with light Bakken crude produced domestically. Canada is the only foreign oil supplier into the Rocky Mountains, now making up about half of the region’s total refinery feedstock. The PADD 4 area is served by Enbridge’s Express Pipeline, which is planned to be expanded from the current 280,000 barrels per day to 330,000 barrels per day. (Oil Sands Magazine, 2020)

PADD 5 refining capacity has fallen from 2.7 million barrels per day in 2000 to under 2.6 million barrels per day in 2019, a decrease of nearly 6 per cent. According to OSM,

Washington State refineries are currently served by the Trans Mountain Pipeline, while California refineries get Canadian crude by oil tanker, with additional volumes supplied by rail. California refineries are geographically cut-off from domestic supplies, relying mostly on overseas imports, blended with heavy oil volumes produced within the state. The region is likely to purchase more Canadian crude when the Trans Mountain Expansion is completed. (Oil Sands Magazine, 2020)

Imports of Canadian crude oil to U.S. PADDs for processing have risen by over 2.5 million barrels per day, or 194% in the past two decades

Overall, Canadian crude oil imports to PADDs for processing have risen from over 1.3 million barrels per day in 2000 to over 3.8 million barrels per day in 2019, an increase of 183 per cent (see Figure 3).

Source: US Energy Information Administration, 2020a.

Oil imports to U.S. PADDs from Canada

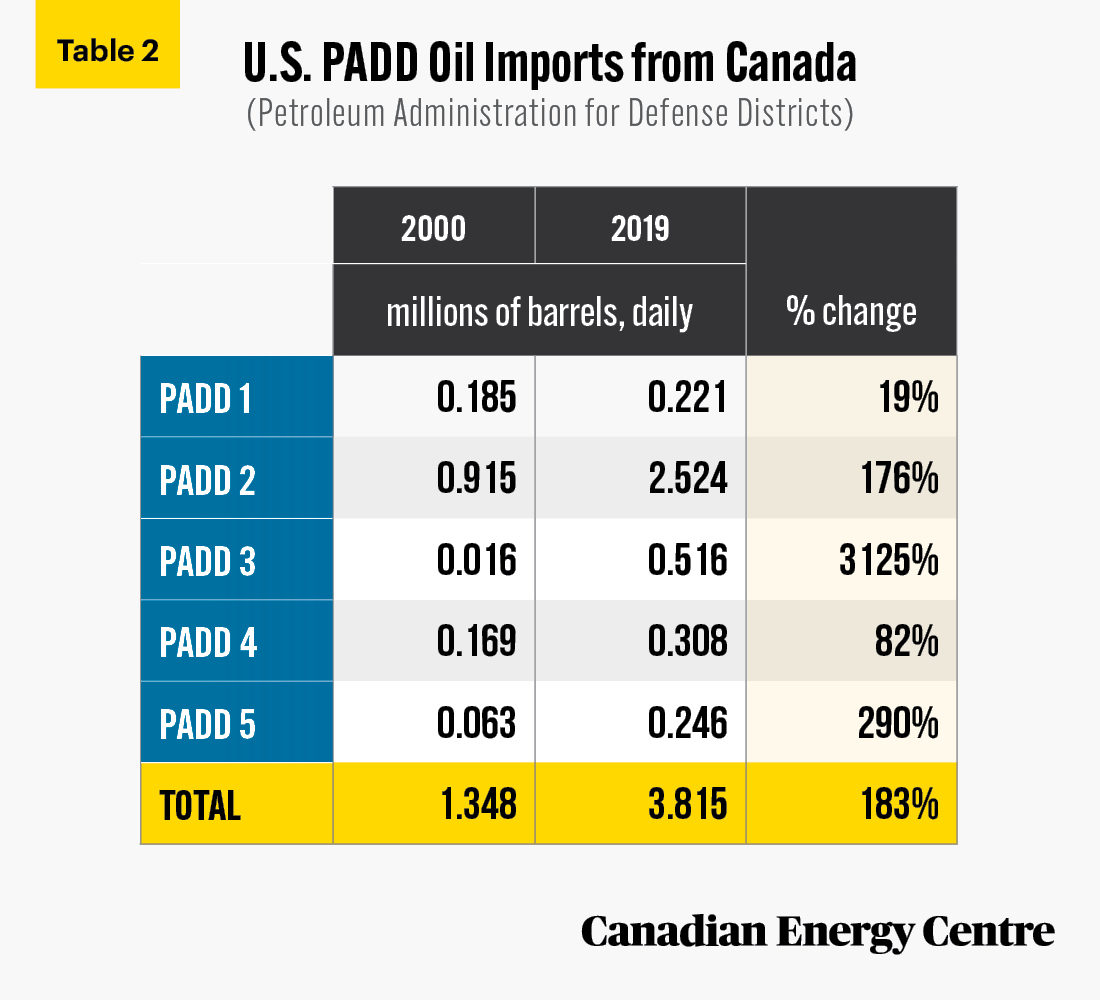

The breakdown of PADD oil imports from Canada is as follows:

- PADD 1: U.S. East Coast oil imports from Canada have risen from 185,000 barrels per day in 2000 to 221,000 barrels per day in 2019, an increase of over 19 per cent. Nearly 32 per cent of foreign oil imports into PADD 1 are now from Canada, up from 12 per cent in 2000.

- PADD 2: U.S. Midwest imports have risen from 915,000 barrels per day in 2000 to 2.5 million barrels per day in 2019, an increase of nearly 176 per cent. Nearly 100 per cent of foreign oil imports into PADD 2 are now from Canada, up from 60 per cent in 2000.

- PADD 3: U.S. Gulf Coast oil imports from Canada have risen from 16,000 barrels per day in 2000 to 516,000 barrels per day in 2019, an increase of 3,125 per cent. Over 26 per cent of foreign oil imports into PADD 3 are now from Canada, up from 3 per cent in 2000.

According to the EIA,

Canada’s exports tend to be heavy crude oil, which Gulf Coast refiners are well equipped to process. Because most new U.S. crude oil production is light and sweet, many Gulf Coast refineries import heavier crude oils such as WCS (Canada’s primary export-grade crude oil) which is considered heavy and sour… Due to the lack of progress on Keystone XL over the past decade, increasing volumes of Canadian crude oil have been transported to PADD 3 via rail (a more expensive option than via pipeline) because the existing pipelines have largely reached their capacities. This capacity limitation has created a transportation constraint and contributed to large price differentials between Western Canadian Select (WCS) and West Texas Intermediate (WTI) crude oil (U.S. Energy Information Administration, 2019).

- PADD 4: U.S. Rocky Mountains oil imports from Canada have risen from 169,000 barrels per day in 2000 to 308,000 barrels per day in 2019, an increase of 82 per cent. One hundred per cent of foreign oil imports into PADD 4 are from Canada, unchanged from 2000.

- PADD 5: U.S. West Coast oil imports from Canada have risen from 63,000 barrels per day in 2000 to 246,000 barrels per day in 2019, an increase of over 290 per cent. Over 19 per cent of foreign oil imports into PADD 5 are now from Canada, up from 9 per cent in 2000.

Every region in the United States is using more Canadian oil now than in 2000, even PADD 5, which has seen its overall processing capacity decline in that time.

Source: U.S. Energy Information Administration, 2020b.

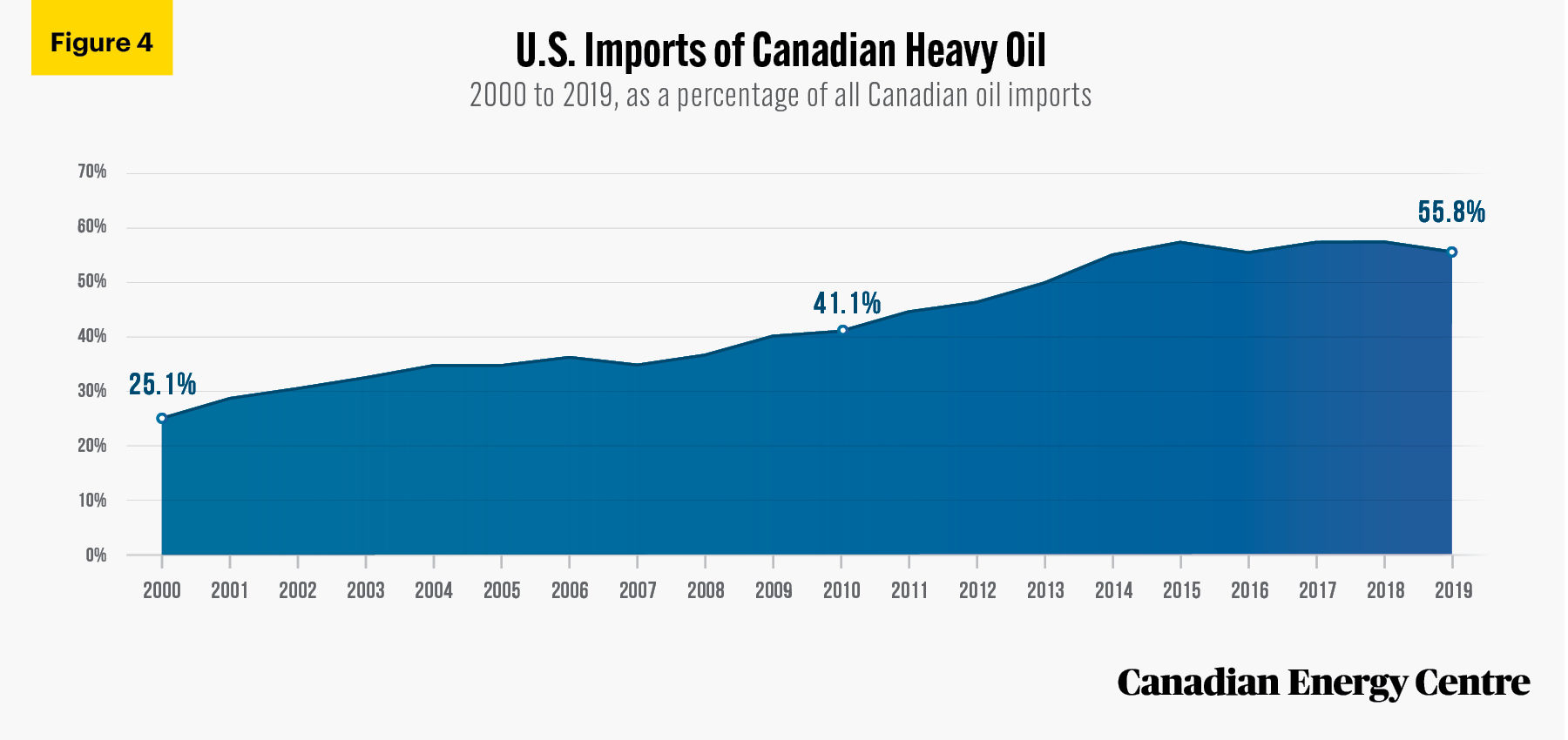

U.S. refineries are increasingly reliant on Canadian heavy oil, including oil from the oil sands: 56% reliance on heavy oil by 2019, up from 25% in 2000

According to Oil Sands Magazine, total U.S. crude output has risen significantly over the past two decades, mostly due to the rise of tight oil production from shale plays, beginning in 2008. Tight oil has a relatively high API density, making it much lighter than conventional oil.

The U.S. domestic supply of crude is becoming increasingly lighter, approaching 40 degrees on the API scale, creating a mismatch with the desired refinery feedstock density, which averages about 32 degrees.

Demand for heavier grades of crude has therefore increased, as refineries seek to blend light domestic crude with heavy and medium grade oil imports (Oil Sands Magazine, 2020).

Although the U.S. has been producing record levels of domestic crude oil, it nonetheless continues to import crude because of variations in crude oil quality. API gravity, along with sulfur content, determines the type of processing needed to refine crude oil into fuel and other petroleum products, all of which factor into refineries’ profits.

By adding imported heavy crude oil to domestic light crude oil in the production process, the U.S. has significantly increased its ability to export refined product. U.S. crude oil exports have increased since the restrictions on exporting domestically produced crude oil were lifted in December 2015.

The percentage of total imports of Canadian heavy oil to the U.S. (i.e., with an API Gravity of 25.0 degrees or less) has risen from 25.1 per cent in 2000 to 55.8 per cent in 2019, an increase of 122 per cent over the past two decades (see Figure 4). According to OSM,

PADD 3 U.S. Gulf Coast remains the prime customer for Canada’s heavy oil producers, including diluted bitumen from the oil sands. The region’s refineries are best designed to handle heavy sour grades, offering the best purchase prices for the world’s heavy oil benchmarks. Almost 100% of Canadian crude oil exports into the U.S. Gulf Coast are heavy. This is precisely why completion of Keystone XL is of critical importance to a region with refineries that are hungry for heavy crude feedstock. (Oil Sands Magazine, 2020)

Source: US Energy Information Administration, 2020a.

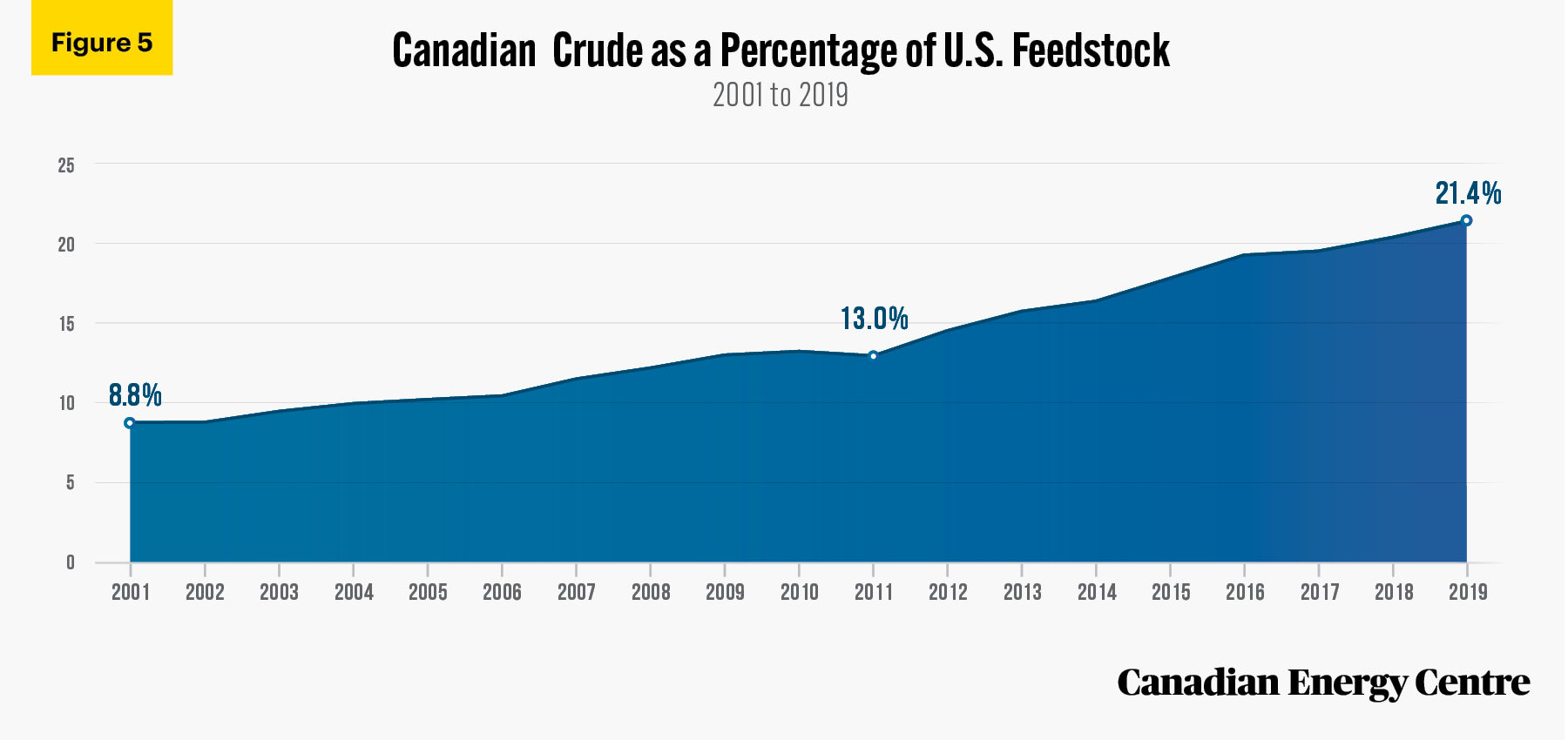

Canadian crude in U.S. refinery feedstock has risen steadily over the past two decades from nearly 9% to over 21%

According to the EIA, U.S. refineries rely on imports as feedstock to optimize production and maximize profits. The refineries process heavy and medium crude oils efficiently and would likely be underutilized if a refinery chose to run only domestically produced light crude oil because the processing plants are designed to convert heavy, low-value intermediate crudes into high-value naphtha and distillates.

In addition to the differences in crude oil quality, the cost to the refiner of acquiring crude oil can be different for domestic and imported crude. The refiner acquisition cost is the total amount that a refiner can expect to pay for crude oil, including freight costs and other transportation fees. Traditionally, heavy and medium crude oils trade at a discount to light, sweet crude oils. Since 2012, the increase in the share of imported crude oils with lower API gravity (heavier oil) has resulted in a lower refiner acquisition cost for imported crude oil when compared with the domestically produced higher API gravity (lighter oil) volumes (U.S. Energy Information Administration, 2020c).

The per cent of Canadian crude in U.S. refinery feedstock (i.e., the raw materials and intermediate materials processed at refineries to produce finished petroleum products, otherwise known as refinery inputs) has steadily risen from nearly 9 per cent in 2000 to over 21 per cent by the end of 2019 (see Figure 5).

Sources: U.S. Energy Information Administration, 2020b and 2021b.

Canadian crude as a percentage of U.S. feedstock, by PADD

Broken down by PADD region (see Table 3),

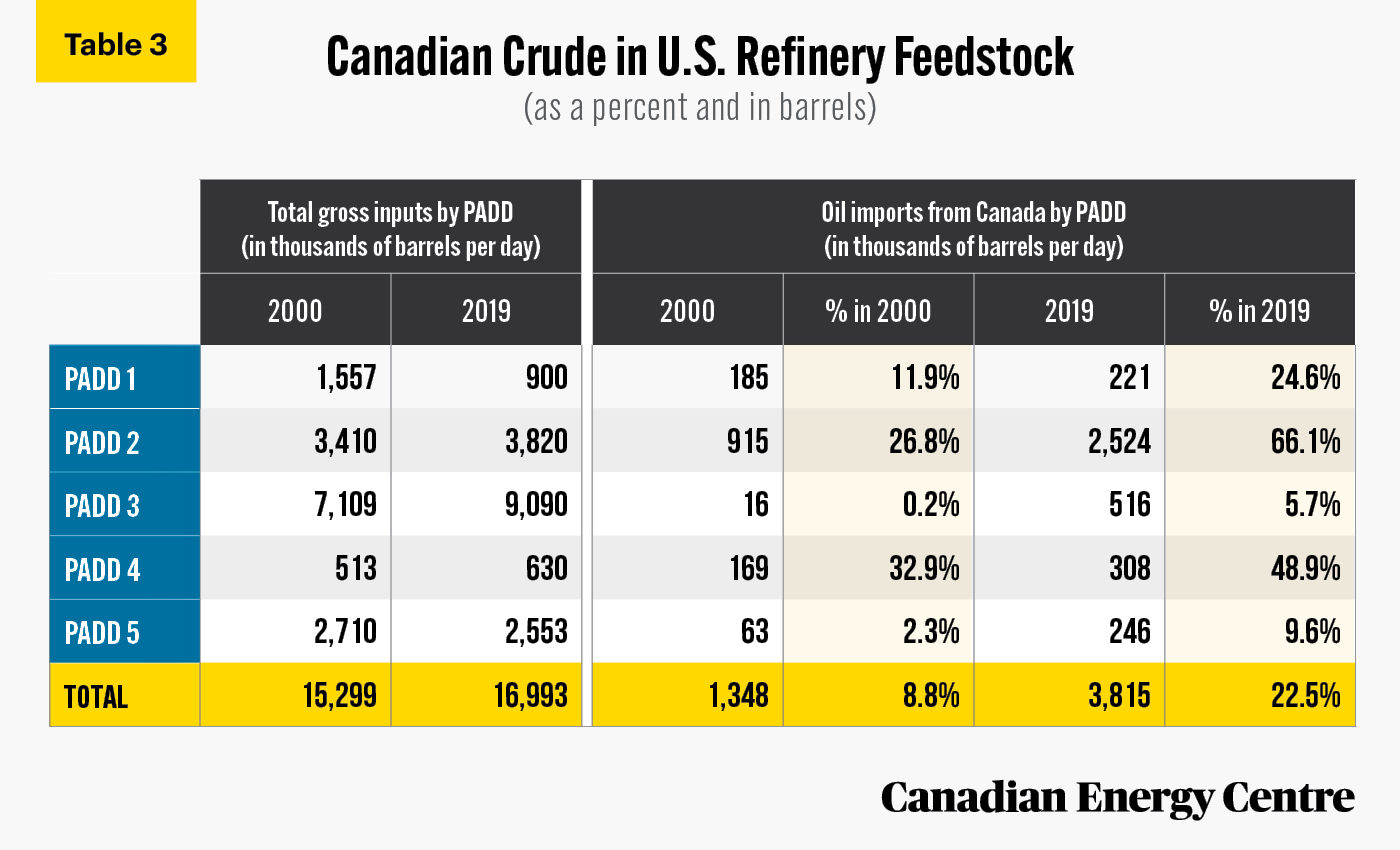

- PADD 1 refineries on the U.S. East Coast processed 24.6 per cent Canadian feedstock in 2019, up from 11.9 per cent in 2000;

- PADD 2 refineries in the U.S. Midwest processed 66.1 per cent Canadian feedstock in 2019, up from 26.8 per cent in 2000;

- Canada still represents only 5.7 per cent of PADD 3 US Gulf Coast refinery feedstock, up from 0.2 per cent in 2000, and thus there are opportunities for Canada to supply more heavy crude to that PADD. According to OSM,

if the Keystone XL pipeline were completed, Canadian feedstock to PADD 3 could rise to as much as 15 per cent. PADD 3 could receive additional volumes of Canadian heavy crude by rail or by pipeline from PADD 2 (Oil Sands Magazine, 2020).

- PADD 4 refineries in the U.S. Rocky Mountains processed 48.9 per cent Canadian feedstock in 2019, up from 32.9 per cent in 2000. As OSM notes,

the PADD 4 area is served by Enbridge’s Express Pipeline, which is planned to be expanded from the current 280,000 barrels per day to 330,000 barrels per day. That should increase the amount of Canadian crude consumed in PADD 4 (Oil Sands Magazine, 2020).

- PADD 5 represents another prime point of entry for Canadian heavy crudes, particularly with the completion of TMX. As of 2019, about 9.6 per cent of PADD 5 refinery feedstock is Canadian, mostly processed in Washington State refineries, up from 2.3 per cent in 2000. According to OSM,

California refineries are geographically cut off from domestic supplies. They rely mostly on overseas imports, which they blend with heavy oil volumes produced within the state. The region is likely to purchase more Canadian crude when the TMX is completed (Oil Sands Magazine, 2020).

Source: U.S. Energy Information Administration, 2020b, 2021b.

Conclusion

According to the American Petroleum Institute and Wood MacKenzie,

America’s refiners are a strategic asset for the United States and maintaining a viable domestic refining industry is critical to the nation’s economic security… Domestic refineries are competing directly with petroleum product imports. Because the refining industry operates on a global basis, America faces the choice of either manufacturing these products at home or importing them from other countries. U.S. refinery closures would result in domestic job losses and lower government revenue in the form of taxes. It would also result in a greater reliance on foreign refineries, such as those being developed in the Middle East and India. (American Petroleum Institute and Wood MacKenzie, 2011)

Continuing to build pipeline infrastructure, such as TMX and Keystone XL, is critical to maintaining a strong U.S. refining industry and increasing Canadian crude oil market share, particularly in PADD 3: U.S. Gulf Coast and PADD 5: U.S. West Coast, both of which are configured to process Canadian heavy oil.

Failure to increase U.S. refining capacity, which also means ensuring the refiners have greater access to Canadian crude oil supplies, will increase American dependence on crude oil imports from less-free countries and risk North American energy security.

References (as of May 12, 2021)

American Petroleum Institute (2021). U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits. <https://bit.ly/3dHng1A>.

American Petroleum Institute and Wood MacKenzie (2011). Outsourcing US Refining? The Case for a Strong Domestic Refining Industry. <https://bit.ly/2NfxPzz>.

IBIS World (2020). Petroleum Refining in the U.S. – Employment Statistics 2005–2026. <https://bit.ly/2QdYqP8>.

Oil Sands Magazine (2020). Market Insights: Assessing America’s Appetite for Canada’s Crude: Canadian Crude Usage by U.S. Refineries, 2020. <http://bit.ly/3aSWAtl>.

U.S. Bureau of Economic Analysis (2021). Industry Economic Account Data: GDP by Industry. <http://bit.ly/3a7hJ3S>.

U.S. Bureau of Labor Statistics (2020a). May 2019 Occupational Employment and Wage Estimates, 2019. <https://bit.ly/3uNdzG6>.

U.S. Bureau of Labor Statistics (2020b). May 2019 Occupational Employment and Wages, Petroleum Pump System Operators, Refinery Operators, and Gaugers. <https://bit.ly/3uLzNZi>.

U.S. Energy Information Administration (2019). U.S. Gulf Coast crude oil imports from Canada reach record-high volumes, This Week in Petroleum. <http://bit.ly/3jDHZ8Z>.

U.S. Energy Information Administration (2020a). PADD District Imports by Country of Origin. <https://bit.ly/3tGRgBF>.

U.S. Energy Information Administration (2020b). Refinery Utilization and Capacity. <https://bit.ly/32Au8IX>.

U.S. Energy Information Administration (2020c). U.S. crude oil production increases; imports remain strong to support refinery operations. <https://bit.ly/3aa6rMp>.

U.S. Energy Information Administration (2021a). Percentages of Total Imported Crude Oil by API Gravity. <https://bit.ly/3n9zSD4>.

U.S. Energy Information Administration (2021b). PAD District Imports by Country of Origin. <https://bit.ly/2Pda7Fq>.

CEC Research Briefs

Canadian Energy Centre (CEC) Research Briefs are contextual explanations of data as they relate to Canadian energy. They are statistical analyses released periodically to provide context on energy issues for investors, policymakers and the public. The source of profiled data depends on the specific issue.

About the authors

This CEC Research Brief was compiled by Lennie Kaplan, Chief Research Analyst at the Canadian Energy Centre and Mark Milke, Executive Director of Research for the Canadian Energy Centre.

Acknowledgments

The Canadian Energy Centre (CEC) would like to thank Oil Sands Magazine and its staff for the genesis of this Research Brief and for providing assistance in interpreting their March 2020 U.S. refinery data set. The authors and the Canadian Energy Centre would like to thank and acknowledge the assistance of Philip Cross in reviewing the data for this Research Brief.

Creative Commons Copyright

Research and data from the Canadian Energy Centre (CEC) is available for public usage under creative commons copyright terms with attribution to the Canadian Energy Centre. Attribution and specific restrictions on usage including non-commercial use only and no changes to material should follow guidelines enunciated by Creative Commons here: Attribution-NonCommercial-NoDerivs CC BY-NC-ND.

Photo Credits

Oil worker courtesy of Government of Alberta, Canada Flag by Igor Kyryliuk, Oil refinery by Nicola Giordano, Oil refinery by Dimitry Anikin, New York Satellite view by NASA, Shipping port by Pixabay, Railyard by Avi Waxman, Pipes by Martin Adams, Freeway by Samuel Agbetunsin.