Social

To sign up to receive the latest Canadian Energy Centre research to your inbox email: research@canadianenergycentre.ca

Download the PDF here

Download the charts here

Introduction

In this CEC Fact Sheet, we examine trends in the total value (expressed in euros) of natural gas imports from within and outside of the European Union (EU) from Not Free, Partly Free, and Free countries¹ between 2005 and 2019.² Despite discussions about diversifying its natural gas supply, countries in the EU continue to import significant quantities of natural gas from autocracies and tyrannies, most notably from Russia.

Germany is considered one of the world’s largest importers of natural gas, with imports mainly coming from the Netherlands, Norway, and Russia (with Russian natural gas imports arriving via Nord Stream). However, the value of natural gas imported into the EU between 2005 and 2019 is derived from Eurostat and is understated as the organization (Eurostat) does not include Germany and France for reasons

of confidentiality.

Nonetheless, according to Rystad Energy, a Norway-based energy research and business intelligence company, data from the last complete year, 2019, shows that Germany – acting also as a gas transport hub – imported 55.5 billion cubic metres (bcm) of gas from Russia, 27 bcm from Norway, and 23.4 bcm from the Netherlands. In total, the three countries accounted for 92 per cent of German gas imports (Rystad Energy, 2020).

It should also be noted that as a Not Free country, Russia has a history of interrupting natural gas flows for political gain. Its behaviour provides Canada with an opportunity to become a reliable supplier of natural gas to the EU.

1. The term “Not Free” is from the Washington DC-based think tank, Freedom House, which has measured and ranked countries and territories by their degree of freedom since 1973. Their broad rankings are: Free, Partly Free, and Not Free. Not Free countries are those where civil and other rights are often far below those of Free countries (Freedom House, 2020). The nine Not Free countries in this Fact Sheet are Algeria, China, Egypt, Iraq, Libya, Russia, Turkmenistan, Turkey, and Uzbekistan. The four Partly Free countries are Morocco, Pakistan, Ukraine, and Serbia. 2. Extra-EU refers to countries outside of the EU. Intra-EU refers to countries within the EU.

EU natural gas imports by value from 2005 to 2019: Over €286 billion from Not Free countries

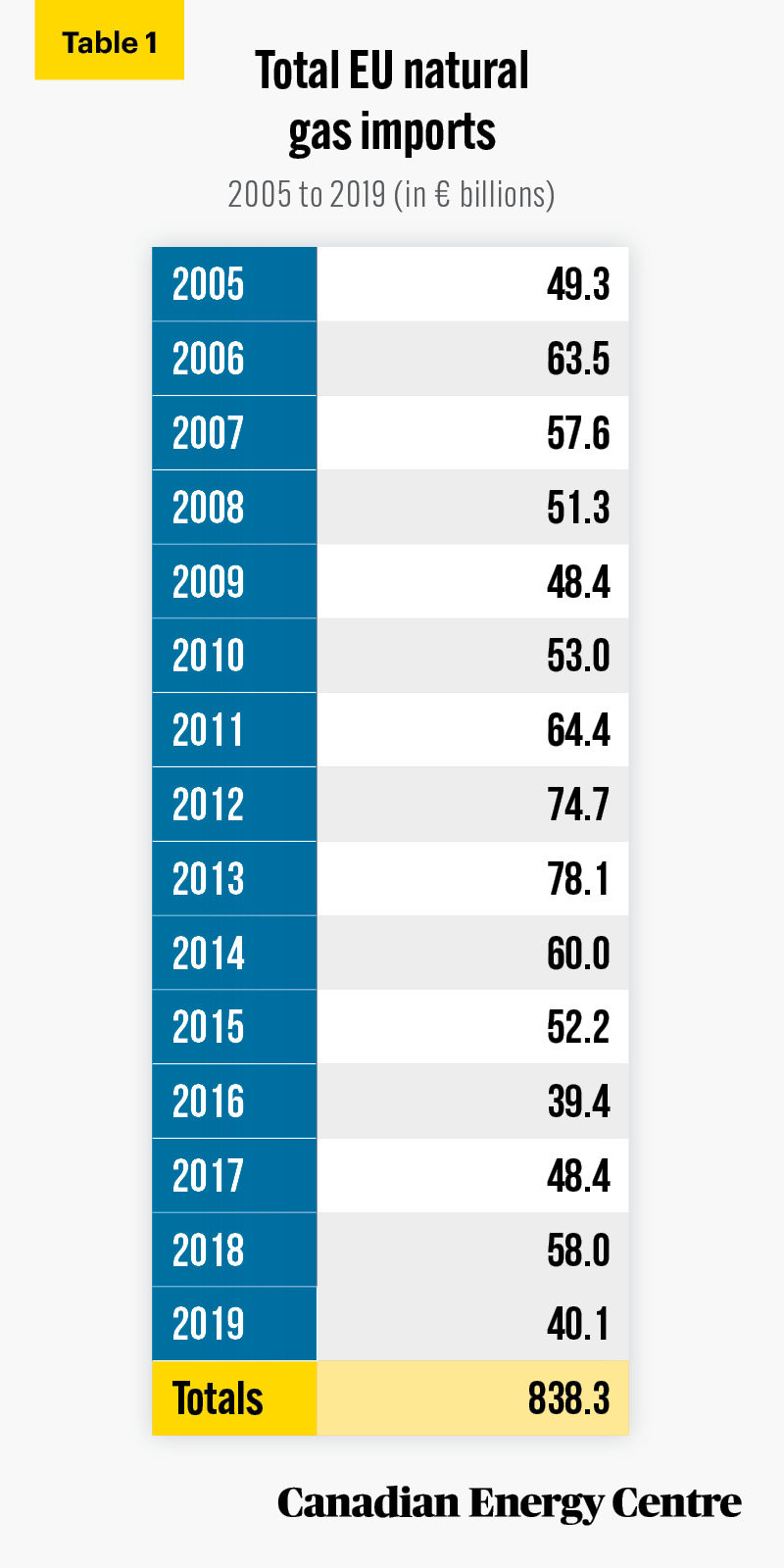

In the past 15 years, the EU has imported €838.3 billion in natural gas from foreign sources, an average of nearly €56 billion per year (see Table 1).

Source: Eurostat, 2021.

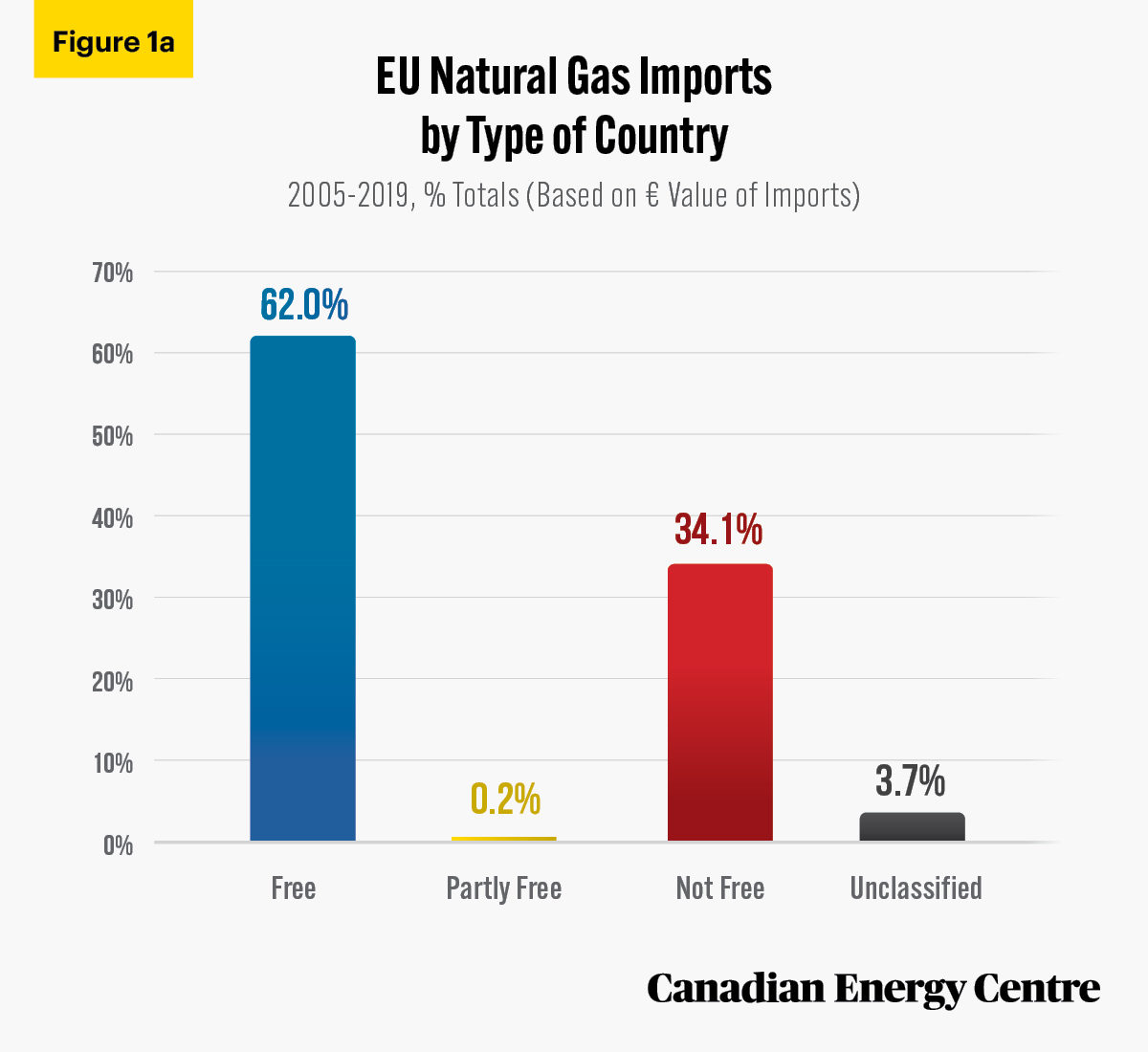

Natural gas valued at over €286 billion, or 34.1 per cent, has been imported from Not Free countries, €519 billion or 62 per cent from Free countries, with an additional €2 billion, or 0.2 per cent, from Partly Free countries (see Figure 1a).

Sources: Eurostat, 2021, and Freedom House, 2020.

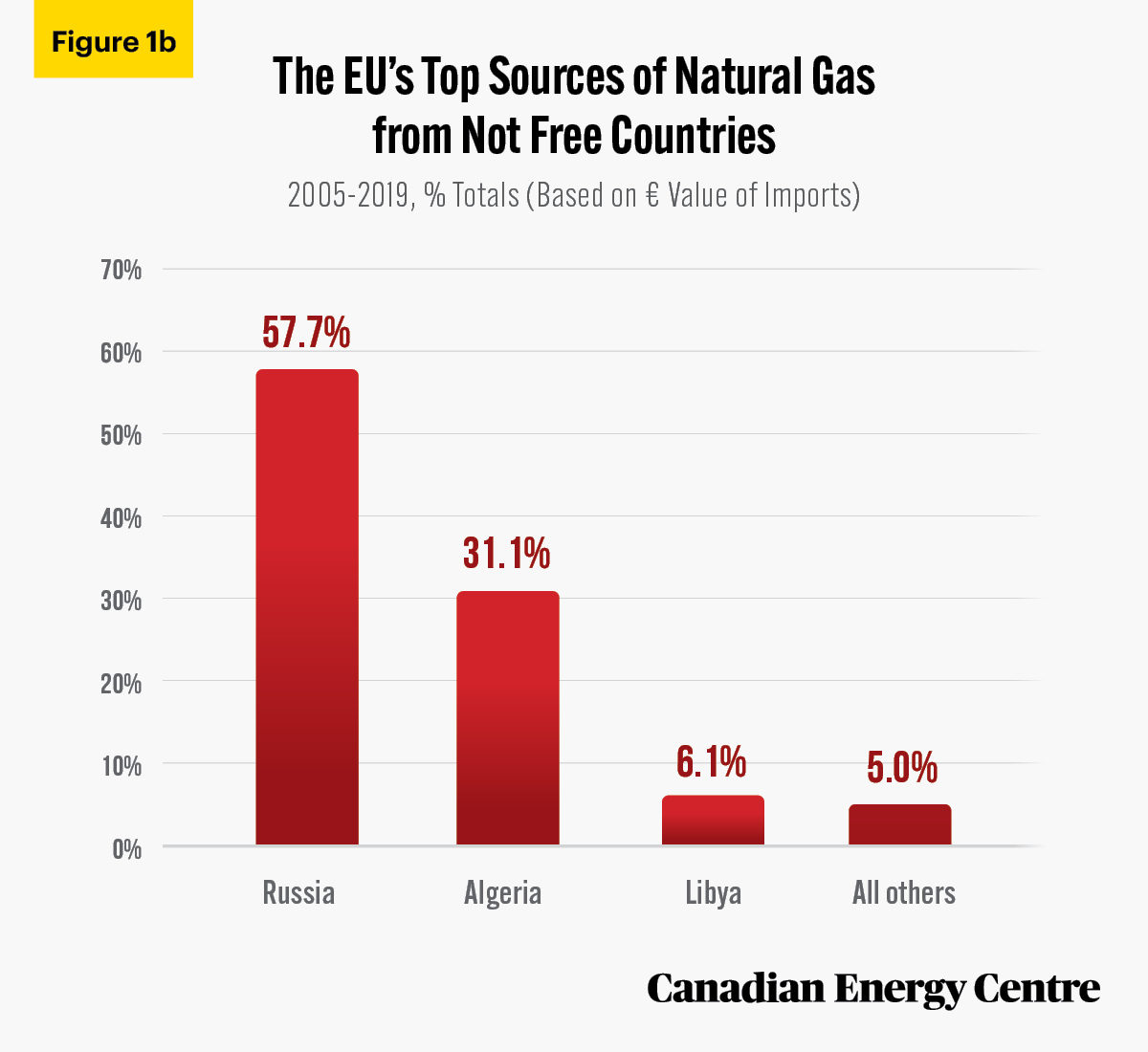

Of the over €286 billion worth of natural gas imported by the EU from Not Free countries between 2005 and 2019,

- almost €165.3 billion worth, or almost 58 per cent, came from Russia;

- over €89.1 billion worth, or 31.1 per cent, came from Algeria;

- and nearly €17.5 billion worth, or 6.1 per cent, came from Libya (see Figure 1b).

Sources: Eurostat, 2021, and Freedom House, 2020.

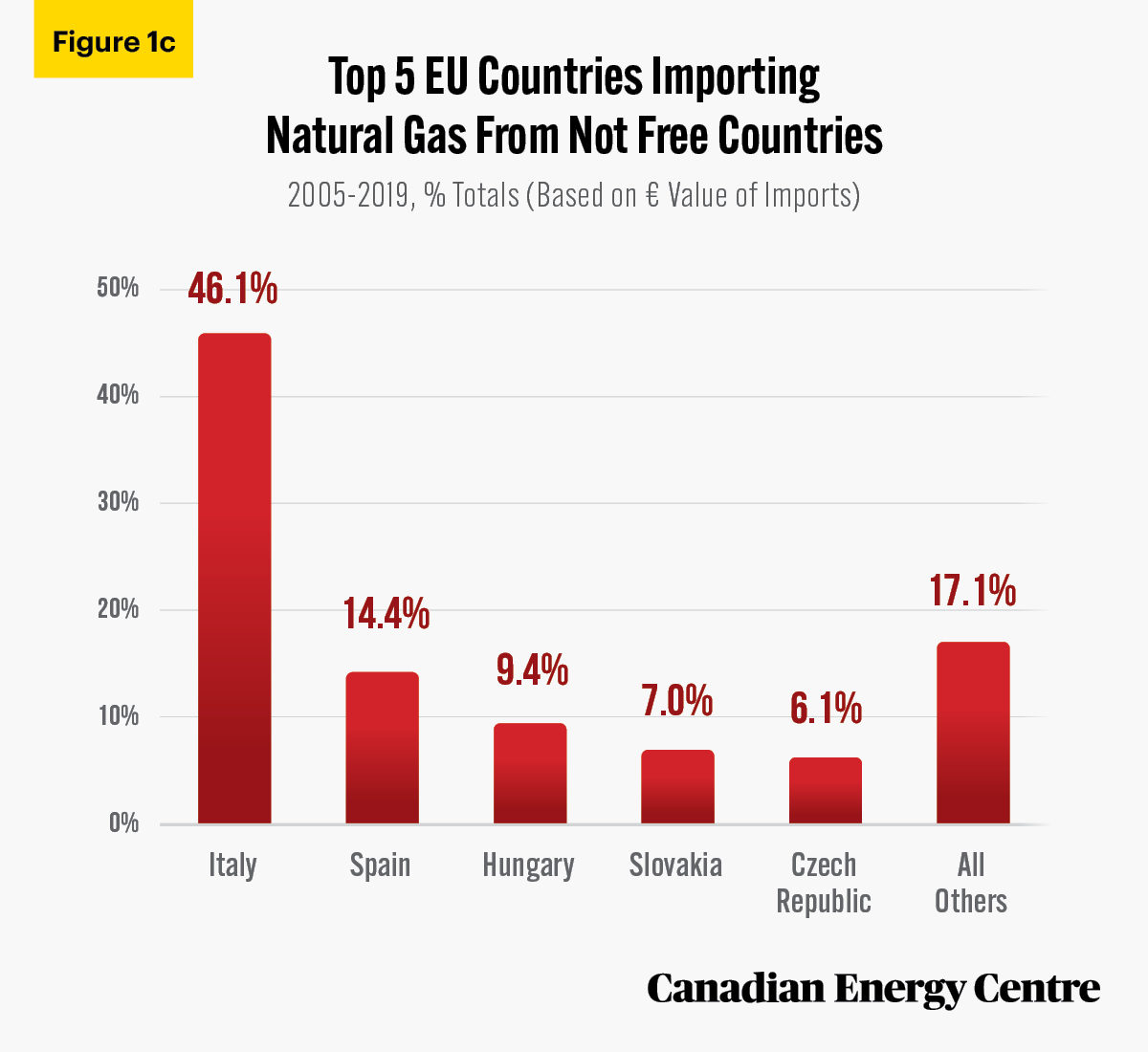

Of the over €286 billion worth of natural gas imported by the EU from Not Free countries between 2005 and 2019,

- Just over €237.1 billion, or nearly 83 per cent, wasimported by Italy, Spain, Hungary, Slovakia, and the Czech Republic.

- Italy led the group at €131.9 billion worth (46.1 per cent)of imported natural gas, followed by Spain at €41.1 billionworth (14.4 per cent), Hungary at nearly €26.8 billion worth (9.4 per cent), Slovakia at €19.9 billion worth (7 per cent), and the Czech Republic at €17.5 billion worth (6.1 per cent) (see Figure 1c).

Sources: Eurostat, 2021, and Freedom House, 2020.

EU natural gas imports in 2019, by value and reporting country

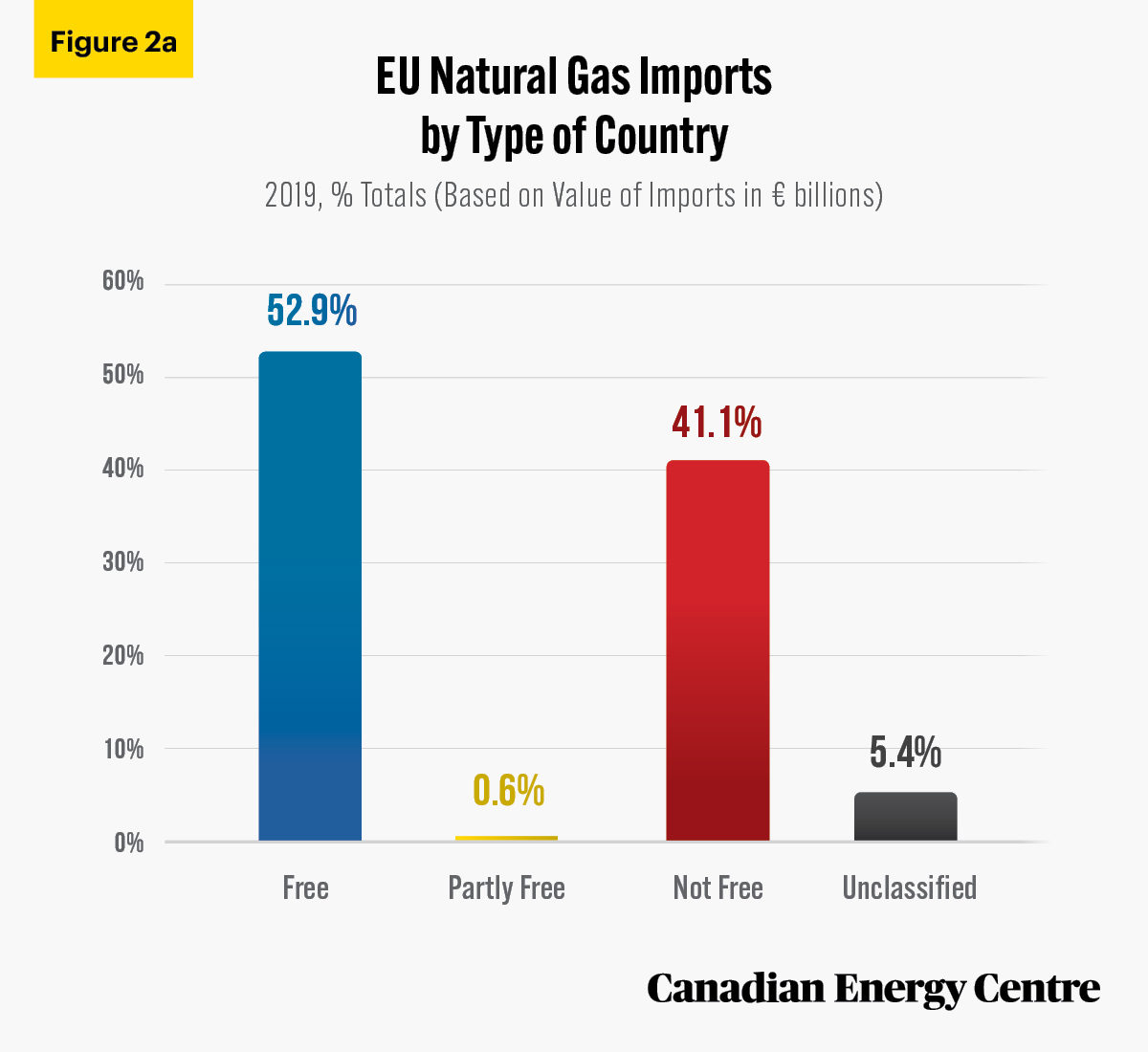

In 2019, the EU imported €40.1 billion in natural gas from outside sources (see Table 1).

Of the €40.1 billion, nearly €16.5 billion, or over 41 per cent, was imported from Not Free countries, €21.2 billion or just under 53 per cent from Free countries, with just another 0.6 per cent from Partly Free countries (see Figure 2a).

Sources: Eurostat, 2021, and Freedom House, 2020.

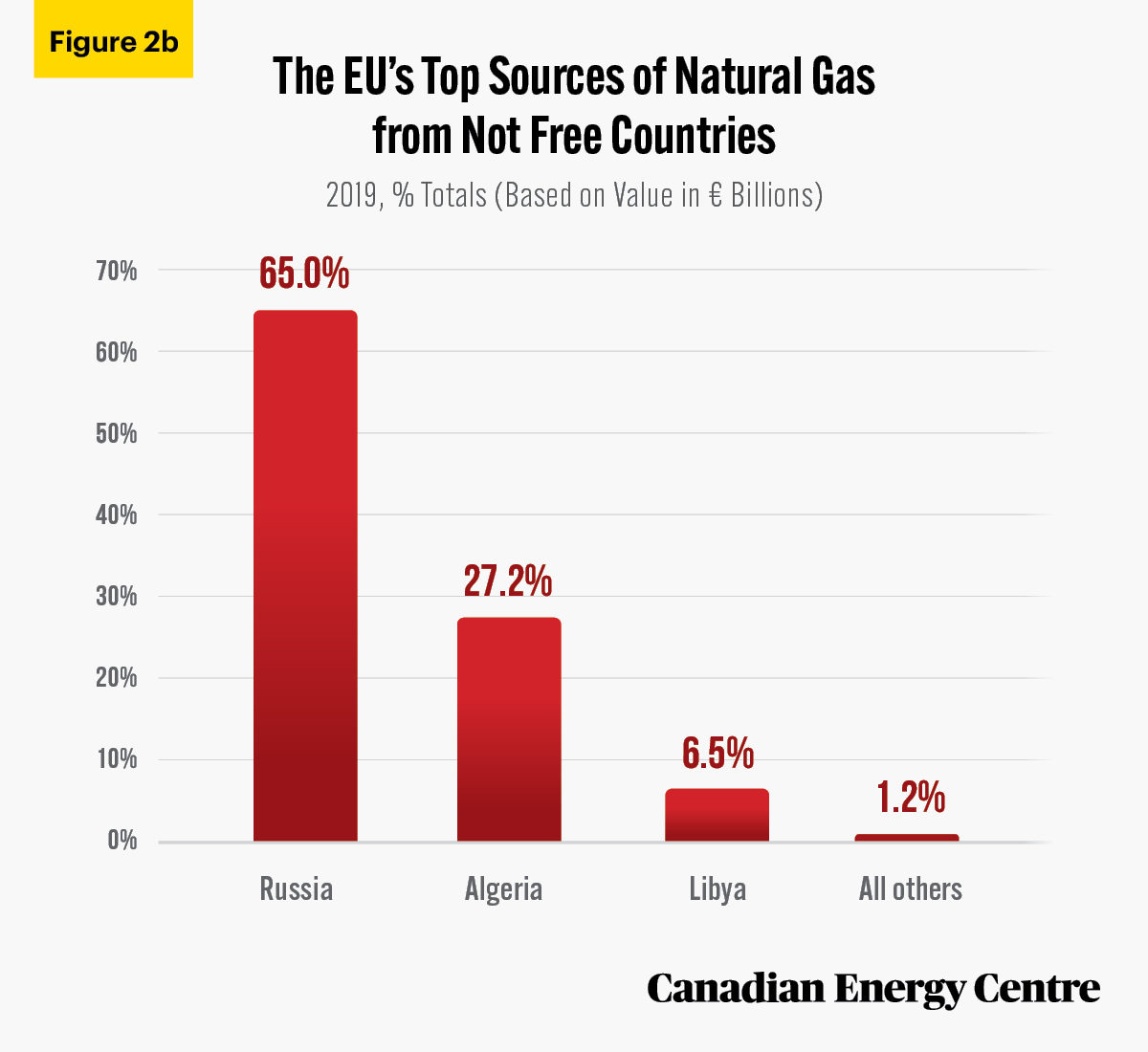

Of the €16.4 billion worth of natural gas that the EU imported from Not Free countries in 2019, nearly €16.3 billion worth, or 99 per cent, was imported from just three countries — Russia, Algeria, and Libya (see Figure 2b).

- over €10.7 billion worth, or 65 per cent, came from Russia;

- nearly €4.5 billion worth, or just over 27 per cent came from Algeria;

- and nearly €1.1 billion worth, or 6.5 per cent, came from Libya (see Figure 2b).

Sources: Eurostat, 2021, and Freedom House, 2020.

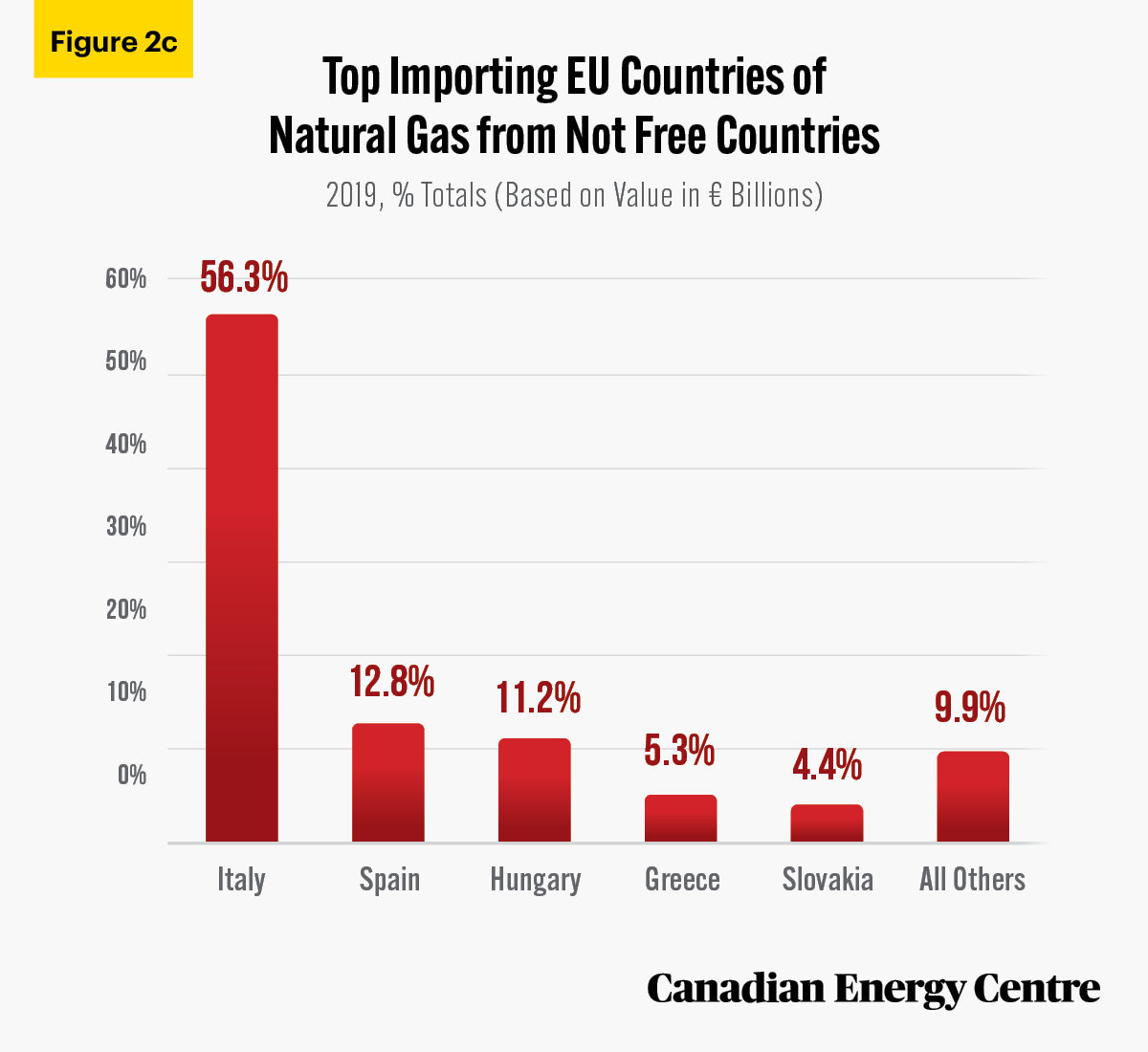

Of the €16.4 billion worth of natural gas that the EU imported from Not Free countries in 2019, Italy, Spain, Hungary, Greece, and Slovakia alone imported over €14.8 billion from tyrannies and autocracies.

- Italy imported the most at nearly €9.3 billion or 56 per cent,

- followed in a distant second by Spain at €2.1 billion or 13 per cent,

- then Hungary at €1.9 billion or 11 per cent,

- followed by Greece at €879 million or 5 per cent, and

- finishing with Slovakia at nearly €718 million or 4 per cent (see Figure 2c).

Sources: Eurostat, 2021, and Freedom House, 2020.

EU and Turkey heavily reliant on Russia for natural gas: 77 per cent of natural gas exports from Russia’s majority state-owned Gazprom go to the EU

As noted earlier, for the past 15 years Russia has been the largest source of natural gas for the EU, exporting over €165 billion worth to the EU in that period. The EU’s dependence on Russia’s natural gas increased when the first of two Nord Stream pipelines, partially owned by Russia’s majority state-owned natural gas company Gazprom, became fully operational in 2012. The pipeline delivers 55 billion cubic metres (bcm) of gas annually from Russia directly to Germany via a pipeline that runs under the Baltic Sea. These deliveries are expected to grow further, by up to another 55 bcm annually, when the second pipeline, Nord Stream 2, becomes operational in 2022. Nord Stream 2 will also run under the Baltic Sea and is seen as “particularly important now when Europe sees a decline in domestic gas production and an increasing demand for imported gas” (Gazprom, undated).

This ever-growing dependence on Russia makes the EU potentially vulnerable to natural gas supply disruptions that could result from geo-political events, such as Russian meddling in the former Soviet Bloc countries. In the past, Russia has punished European countries that were selling Russian gas to Ukraine by cutting off natural gas being delivered through both Nord Stream and an existing pipeline to the Ukraine.

According to Marcus Kolga of the MacDonald-Laurier Institute,

Nord Stream 2 will allow Russia to consolidate much of its gas exports directly to Germany as a transit country, thereby making European energy supplies heavily dependent on Russia-German relations. Indeed, (Vladimir) Putin would be able to quickly cut a significant portion of its natural gas to Europe on just this one route. Equally important is that Russia will be able to significantly reduce its gas exports through Ukraine. This will remove an important link between Ukraine and the rest of Europe, while also leaving Ukraine and Poland at a disadvantage – both financially with declining transit revenues, but also in any future gas negotiations with Russia energy giant Gazprom (Kolga, 2019).

Gazprom is already by far the largest supplier of gas to Europe. In 2019, Gazprom supplied nearly 199 bcm of gas to European countries. Western European countries and Turkey accounted for approximately 77 per cent of the company’s exports, while Central European states took 23 per cent (Gazprom, 2021). More specifically,

- Germany used the most gas at 57 bcm

- followed by Italy at just over 22 bcm

- Austria took nearly 16.3 bcm,

- Turkey used 15.5 bcm,

- France bought nearly 14.1 bcm,

- the United Kingdom procured 10.3 bcm,

- Hungary took nearly 11.3 bcm, and

- Poland received just over 9.7 bcm (Gazprom, 2021).

Russia is a problematic supplier of natural gas for the EU. Bonnie Saynay, head of Research and Data Strategy for Institutional Shareholder Services (ISS) ESG observed that “Concepts of socially-acceptable policies in Russia, where domestic violence was partially decriminalized in 2017 and ‘homosexual propaganda’ to minors is outlawed, also differ widely from European and U.S. investors’ expectations” (Fedorinova, 2020).

According to Nemanja Popovic, political and economic analyst at the Atlantic Sentinel, “for the long run, the European Union should aim to diversify its supply routes…By diversifying its imports, it can curtail Russia’s influence in its energy markets and limit the severity of potential infrastructural failures” (Popovic, 2020).

Emerging opportunities for Canadian natural gas and LNG to break into the EU supply chain

For at least 15 years the EU has been heavily dependent on the natural gas shipped to it from autocracies and tyrannies, most notably Russia. With the planned completion of Gazprom’s Nord Stream 2, natural gas imports to the EU from Russia will only grow, making the EU even more vulnerable to Russian influence. Canada could help reduce that dependence.

According to Natural Resources Canada, at the end of 2018 Canada had 73 trillion cubic feet (tcf) of proven natural gas reserves (Natural Resources Canada, undated). Through strategic investments in infrastructure, including pipelines and LNG terminals, and a more predictable regulatory regime for investors, Canada could secure new markets for its gas in Europe, thereby helping the EU diversify its gas import markets and reducing its dependence on Russia.

Marcus Kolga of the Macdonald-Laurier Institute sums up Canada’s opportunities this way:

As Alberta desperately seeks new markets for its energy resources and concerns about Western alienation and the threat to federal cohesion grow, Europe’s dangerous, self-inflicted reliance on Russian gas could offer a historic opportunity for Canada… federal and provincial governments would be wise to facilitate the export of Canadian energy to new markets in Europe. Doing so will allow us to advance our economy, address concerns about national unity and reinforce the security of our European NATO allies. (Kolga, 2019

Notes

This CEC Fact Sheet was compiled by Lennie Kaplan and Mark Milke at the Canadian Energy Centre (www.canadianenergycentre.ca). All percentages in this report are calculated from the original data, which can run to multiple decimal points. They are not calculated using the rounded figures that may appear in charts and in the text, which are more reader friendly. Thus, calculations made from the rounded figures (and not the more precise source data) will differ from the more statistically precise percentages we arrive at using source data. The authors and the Canadian Energy Centre would like to thank and acknowledge the assistance of Dennis Sundgaard in reviewing the data and research for this Fact Sheet. Image credits: Patrick Federi from Unsplash.com

References (All links live as of October 5, 2021)

Euroactive (2017), Gazprom says exports to Germany hit record high in 2016 <https://bit.ly/3z3BbIL>; Eurostat (2021), International trade in goods, EU trade since 1988 by HS2,4,6 and CN8 (DS-645593) <http://bit.ly/3eRErQi>; Eurostat (2020), EU imports of energy products – recent developments <http://bit.ly/3eQySBK>; Fedorinova, Yuliya (2020), Russian sustainability scores rise, but climate goal still lags, BNN Bloomberg <http://bit.ly/30TGsmU>; Freedom House (2020), Countries and Territories: Global Freedom Scores <https://bit.ly/2yS1IPf>; Gazprom (2021), Gazprom Exports <http://bit.ly/3cIG7ZF>; Gazprom (Undated), Nord Stream 2 <https://bit.ly/3mc60pn>; Kolga, Marcus (2019), Canada could help Europe diversify its energy supplies from Russia, Macdonald-Laurier Institute <http://bit.ly/2Qgf68t>; Natural Resources Canada (Undated), Natural Gas Facts <http://bit.ly/3jz7jMK>; Popovic, Nemanja (2020), The energy relationship between Russia and the European Union <http://bit.ly/3vDSfUi>; Rystad Energy (2020), Germany’s gas demand to top 110 Bcm by 2034 and Nord Stream 2 is the cheapest new supply option <https://bit.ly/3j0EcE5>; Sustainalytics (2021), Company ESG Risk Ratings: Gazprom PJSC <http://bit.ly/3bU3Oin>.

Creative Commons Copyright

Research and data from the Canadian Energy Centre (CEC) is available for public usage under creative commons copyright terms with attribution to the CEC. Attribution and specific restrictions on usage including non-commercial use only and no changes to material should follow guidelines enunciated by Creative Commons here: Attribution-NonCommercial-NoDerivs CC BY-NC-ND.